Morgan Stanley Sees Chinese Auto Market Recovery Gaining Momentum in Late Summer

Morgan Stanley Sees Chinese Auto Market Recovery Gaining Momentum in Late Summer  UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty

UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty  Stock Futures Dip as Investors Await Key Payrolls Data

Stock Futures Dip as Investors Await Key Payrolls Data  Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close

Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close  Today’s space race could turn fatal if we don’t agree on new rules

Today’s space race could turn fatal if we don’t agree on new rules  Silver Cracks Key 365-Day EMA for First Time Since Feb 2024; Bears Eye $50 on Rallies

Silver Cracks Key 365-Day EMA for First Time Since Feb 2024; Bears Eye $50 on Rallies  SpaceX Stock Gets $175 Target as Analysts See Massive Growth Ahead

SpaceX Stock Gets $175 Target as Analysts See Massive Growth Ahead  Urban studies: Doing research when every city is different

Urban studies: Doing research when every city is different  Gold's 365-Day EMA Streak Since Oct 2023 Faces Its First Real Test at $3,980 — Break or Bounce to $4,140?

Gold's 365-Day EMA Streak Since Oct 2023 Faces Its First Real Test at $3,980 — Break or Bounce to $4,140?  US Gas Market Poised for Supercycle: Bernstein Analysts

US Gas Market Poised for Supercycle: Bernstein Analysts  Fed May Resume Rate Hikes: BofA Analysts Outline Key Scenarios

Fed May Resume Rate Hikes: BofA Analysts Outline Key Scenarios

The Australian inflation data for Q2 provided a considerable dampener for the rate cut speculation this morning.

The inflation measure preferred by the Australian central bank (RBA), the trimmed mean, remained surprisingly stable at 1.7% YoY.

That means, at least on the inflation front the RBA does not see any urgent need for action. The rise of AUD since late May, on the other hand, is likely to be a reason for concerns for the central bank. That means the door has not been completely shut on a rate cut yet.

On the flip side, This week is a busy one for Japan data watchers with many June releases including CPI, housing starts, and FX markets digesting the better than forecasted trade balance data, while the key focus should be on Friday’s BoJ policy meeting.

If it is judged necessary for achieving the price stability target” (from June Statement on Monetary Policy). The economy has struggled with deflation for two decades. Even after the BOJ's massive qualitative and quantitative easing (QQE) program and venture into negative interest rates territory, the Asian economy hasn't been able to boost domestic consumption and shake off deflation.

Hedging Framework: Capitalize on rallies and HY vols likely to favour PRBS

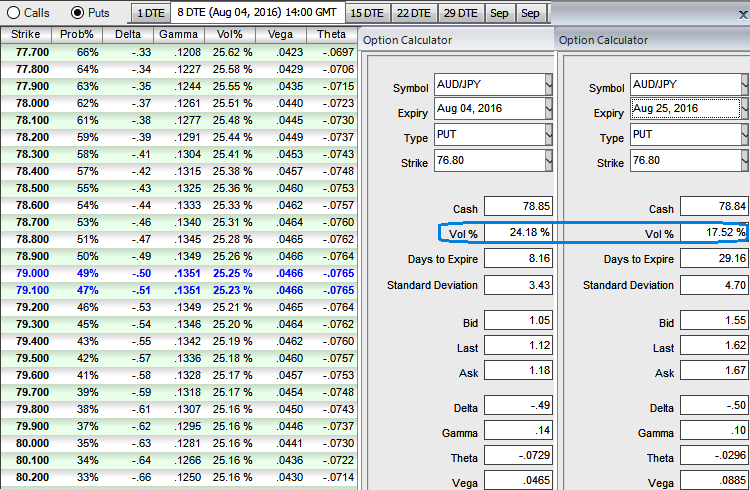

AUDJPY has consistently been sliding in a sloping channel as selling momentum is intensified as the monetary policies adding extra impetus to the selling pressures, so the foreign traders who have their export or import bills should be hedged by below option strategies.

ATM IVs of 1w expiries are flashing at 24.18% and 17.52% for 1m tenor.

While IVs of ATM contracts of 1w and 1m tenors are spiking crazily and this has been justified by historical volatilities in spot FX fluctuations (see big real body candles on monthly technical charts).

Traders tend to view the put ratio back spread as a bear strategy because it employs puts. However, it is actually a volatility strategy. The implied volatility of 1M ATM put contract is at 17.52% and it is quite higher side when long-term trend is bearish.

Traders tend to view the put ratio back spread as a bear strategy because it employs puts. However, it is actually a volatility strategy.

Options with a higher IV cost more. This is intuitive due to the higher likelihood of the market 'swinging' in your favour.

As we expect the underlying currency exchange rate of AUDJPY to make a larger move on the downside. As shown in the figure purchase 1M 2 lots of At-The-Money -0.52 delta puts and sell 1W one lot of (1%) In-The-Money put option.