Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure

Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure  Moldova Criticizes Russia Amid Transdniestria Energy Crisis

Moldova Criticizes Russia Amid Transdniestria Energy Crisis  Urban studies: Doing research when every city is different

Urban studies: Doing research when every city is different  China's Refining Industry Faces Major Shakeup Amid Challenges

China's Refining Industry Faces Major Shakeup Amid Challenges  Trump’s "Shock and Awe" Agenda: Executive Orders from Day One

Trump’s "Shock and Awe" Agenda: Executive Orders from Day One  Bank of America Posts Strong Q4 2024 Results, Shares Rise

Bank of America Posts Strong Q4 2024 Results, Shares Rise  U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures

U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures  Goldman Sachs: US Dollar Likely to Stay Strong Despite Oil Price Retreat

Goldman Sachs: US Dollar Likely to Stay Strong Despite Oil Price Retreat  Geopolitical Shocks That Could Reshape Financial Markets in 2025

Geopolitical Shocks That Could Reshape Financial Markets in 2025  Energy Sector Outlook 2025: AI's Role and Market Dynamics

Energy Sector Outlook 2025: AI's Role and Market Dynamics  How AI prompting turned writerly description into an everyday skill

How AI prompting turned writerly description into an everyday skill  European Stocks Rally on Chinese Growth and Mining Merger Speculation

European Stocks Rally on Chinese Growth and Mining Merger Speculation  Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed

Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed  Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms

Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms

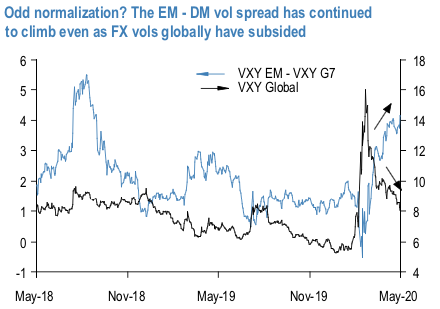

The traditionally fearsome risk-unfriendly May seasonality has come and gone without much of a flutter in FX option markets. FX vols globally continued to melt lower all month, US/China tensions notwithstanding, and by now have retraced 80% of their 1Q’20 spike. The most notable feature of this normalization is that it has been predominantly G7 led, as reflected in a steady climb higher in the EM – DM vol spread over the past two months (refer above chart).

In addition to the continued richness of risk-reversals on vol surfaces across the board, this is the most noteworthy manifestation of lingering nervousness and/or long memory

of the earthquake in financial markets earlier in the year.

The outlook on the macro risk backdrop, and by extension currency volatility gets murky from here. On the one hand, the vol dampening / spread compressing impact of central bank liquidity is in full flow across assets, oil prices have rebounded sharply, and even normalization laggards such as EM FX with more-than-justified indebtedness concerns – and with it the broad dollar – are showing signs of succumbing to the rush of optimism coursing through markets.

At the same time, new risks in the form of a worrying escalation in US/China tensions have surfaced, and value in playing for additional G10 (and especially G3) vol compression has disappeared given the wider disconnect between low vol and poor activity data. These offsets do not lend themselves to high conviction, directional vol views at present, hence our alpha recommendations strive to maintain a semblance of balance between a core collection of vol-surface carry trades cantered on fading rich risk- reversals with a set of defensive relative value constructs.

In the spirit of abstaining from big macro vol calls, we zero in on two relatively micro-distortions in the Yen option complex – a corner of the FX option market that has suffered disproportionately from the ongoing collapse in G3 vol.

First, we propose a low maintenance option construct for fading rich risk-reversal / ATM ratios for investors without the bandwidth to actively hedge deltas.

Second, we highlight the historically anomalous tightness of cross-yen vs. USD-vol spreads with specific reference to GBP, which is susceptible to a potentially turbulent month of Brexit negotiations leading up to the Withdrawal Agreement extension deadline in end-June and worth hedging convexly with GBPJPY – GBPUSD gamma spreads. Courtesy: JPM