Goldman Sachs: US Dollar Likely to Stay Strong Despite Oil Price Retreat

Goldman Sachs: US Dollar Likely to Stay Strong Despite Oil Price Retreat  Urban studies: Doing research when every city is different

Urban studies: Doing research when every city is different  Moldova Criticizes Russia Amid Transdniestria Energy Crisis

Moldova Criticizes Russia Amid Transdniestria Energy Crisis  S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays

S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays  Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms

Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms  US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts

US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts  Gold's 365-Day EMA Streak Since Oct 2023 Faces Its First Real Test at $3,980 — Break or Bounce to $4,140?

Gold's 365-Day EMA Streak Since Oct 2023 Faces Its First Real Test at $3,980 — Break or Bounce to $4,140?  Geopolitical Shocks That Could Reshape Financial Markets in 2025

Geopolitical Shocks That Could Reshape Financial Markets in 2025  Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure

Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure  Today’s space race could turn fatal if we don’t agree on new rules

Today’s space race could turn fatal if we don’t agree on new rules  Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data

Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data

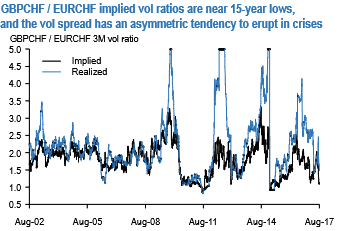

Over the next few months, GBP is likely to continue trading on the back-foot. Sterling may have cheapened considerably since the Brexit referendum in June 2016, but the sizeable current account deficit remains an albatross around its neck, while real UK yields are notably low. Consequently, GBP crosses have also been flashing tepid vols.

GBPCHF – EURCHF vol spreads: GBPCHF vs EURCHF vol ratios are approaching 15-year lows, nearly at par with extremes first witnessed at the height of the EMU crisis in the fall of 2011 that brought on the 1.20 peg in the first place, and then revisited when it was removed two years ago (refer above chart). Owning the vol spread has a desirable positive asymmetry from current levels, a tendency for one-sided eruptions in favor of a wider GBPCHF premium during market crashes, and enjoys small positive carry at inception (2M ATM vol spread 0.7 mid, 1-mo realized vol spread 1.5).

It should not escape attention too that the RV is fairly well-insulated from SNB-shenanigans: chart 7 digs forensically into the return profile of vol spreads initiated every day in the months leading up to and spanning the 2015 de-peg shock, and surmises that the mean return around the episode was positive to the tune of 2 vol pts., with an appreciable positive skewness.

The results are not entirely surprising since GBPCHF’s higher risk-beta compared to EURCHF imparts an anti-risk bias to the spread that manifests in its predictable crash sensitivity in above chart, and is handy in the current context when GBP faces idiosyncratic Brexit risks and unpredictable market reaction to potential BoE rate hikes amid growth weakness. Hence, GBPCHF – EURCHF 2M ATM straddle spreads are advocated @ 0.75/1.0 vol indic. offer. Source: JP Morgan