Stock Futures Dip as Investors Await Key Payrolls Data

Stock Futures Dip as Investors Await Key Payrolls Data  SpaceX Stock Gets $175 Target as Analysts See Massive Growth Ahead

SpaceX Stock Gets $175 Target as Analysts See Massive Growth Ahead  UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data

UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data  Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure

Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure  Trump’s "Shock and Awe" Agenda: Executive Orders from Day One

Trump’s "Shock and Awe" Agenda: Executive Orders from Day One  How AI prompting turned writerly description into an everyday skill

How AI prompting turned writerly description into an everyday skill  Gold's 365-Day EMA Streak Since Oct 2023 Faces Its First Real Test at $3,980 — Break or Bounce to $4,140?

Gold's 365-Day EMA Streak Since Oct 2023 Faces Its First Real Test at $3,980 — Break or Bounce to $4,140?  U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge

U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge  Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms

Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms  AI Memory Boom Sparks Global Chip Supply Crunch

AI Memory Boom Sparks Global Chip Supply Crunch  Geopolitical Shocks That Could Reshape Financial Markets in 2025

Geopolitical Shocks That Could Reshape Financial Markets in 2025  S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays

S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays  UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty

UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty  World Cup technology: from ref cams to AI analysts, cutting-edge research is changing the game

World Cup technology: from ref cams to AI analysts, cutting-edge research is changing the game

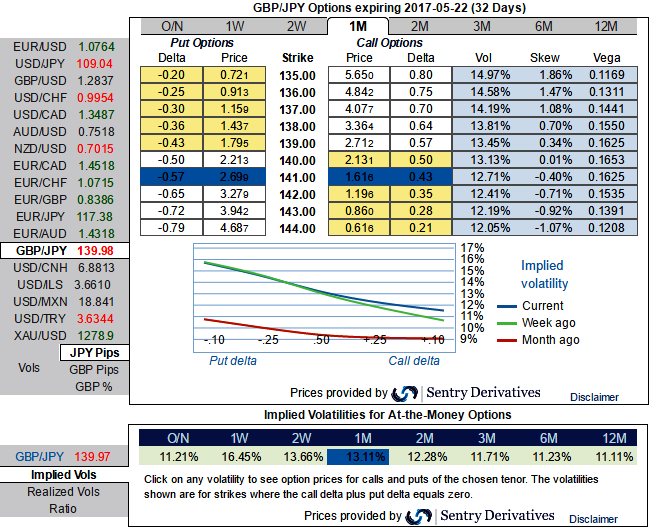

Please be noted that the 1m implied volatilities of GBPJPY are spiking above 13.10%, while positively skewed IVs signifies the hedging interests in OTM put strikes.

In spite of GBPJPY downtrend seems to be intact, a lot of bad news is already priced in and digested by the market. Brexit caused two Sterling debacles, first in June with the vote and then after the summer when PM May suggested a hard exit.

GBPJPY lost over 3-4% over this quarter with one fortnight to spare and it doesn’t seem the dust has settled. In the process, volatility fell but remained relatively high on a historical basis.

Assuming a medium-term range in this pair and that negative surprises are no longer market tail risks, the GBP volatility is still short.

Even if the aggressive volatility investors want to capture GBP should consider buying ATM put instruments and/or being long of the smile convexity, against ATM volatility.

But further GBPJPY weakness and/or abrupt upswings suggests building a directional and volatility patterns at the same time: the value of OTM puts would likely to rise significantly as the IVs seem to be favoring these distant strikes. We, therefore, recommend buying a 1w1m IV skews and risk reversal with ATM options.

Subsequently, since 1m implied volatilities are considerably spiking on higher side that is most likely to favor vega puts in the robust downtrend.

As a result, we believe in jacking up in long leg of the below option strategy:

Initiate longs of 2 lots of 1m at the money vega put options, simultaneously, short 1 lot of (1%) out of the money put of 2w expiry with positive theta. It is advisable to prefer European style options.