Bank of Canada Holds Interest Rate at 2.25% Amid Trade and Global Uncertainty

Bank of Canada Holds Interest Rate at 2.25% Amid Trade and Global Uncertainty  Bank of America Posts Strong Q4 2024 Results, Shares Rise

Bank of America Posts Strong Q4 2024 Results, Shares Rise  US Gas Market Poised for Supercycle: Bernstein Analysts

US Gas Market Poised for Supercycle: Bernstein Analysts  MAS Holds Monetary Policy Steady as Strong Growth Raises Inflation Risks

MAS Holds Monetary Policy Steady as Strong Growth Raises Inflation Risks  BOJ Policymakers Warn Weak Yen Could Fuel Inflation Risks and Delay Rate Action

BOJ Policymakers Warn Weak Yen Could Fuel Inflation Risks and Delay Rate Action  Energy Sector Outlook 2025: AI's Role and Market Dynamics

Energy Sector Outlook 2025: AI's Role and Market Dynamics  Federal Reserve Faces Subpoena Delay Amid Investigation Into Chair Jerome Powell

Federal Reserve Faces Subpoena Delay Amid Investigation Into Chair Jerome Powell  U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?

U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?  RBA Raises Interest Rates by 25 Basis Points as Inflation Pressures Persist

RBA Raises Interest Rates by 25 Basis Points as Inflation Pressures Persist  China's Refining Industry Faces Major Shakeup Amid Challenges

China's Refining Industry Faces Major Shakeup Amid Challenges

Bearish EURNZD Scenarios:

1) ECB goes all-in with rates cuts, tiering and QE.

2) Trump proceeds with tariffs on Euro car imports.

3) A no-deal Brexit.

4) Kiwis fiscal easing is accelerated;

5) Housing begins to lift thanks to lower mortgage rates and a winding back of LVR restrictions.

Bullish EURNZD Scenarios:

1) Trump sanctions unilateral FX intervention to weaken USD.

2) A US-China peace treaty on trade.

3) Euro-area economy rebounds to a sustained 1.5%+ growth rate and re-acceleration of CB demand for EUR.

4) The housing market slowdown becomes deeper due to credit tightening by banks;

5) The immigration rolls over more quickly;

6) The global risk assets start to respond more sharply to global trade and growth concerns.

Today’s event highlight is the ECB’s (European central bank) monetary policy meeting, where a 10bps deposit rate cut to - 0.50% is a common consensus, as well as a QE signal. That could hurt the EUR, following the ECB’s surprisingly dovish message in the recent past. For the eurozone, we have lowered our forecast for 2020 from 1.1% to 0.7% as Germany remains in the grey zone between lean growth and recession. The looming protracted economic slowdown suggests more than ever that the ECB will adopt a comprehensive easing package at its next meeting in September. The ECB should lower its deposit rate from -0.4% to -0.6%, introduce a tiered interest rate system to relieve banks of the penalty interest rate and resume net purchases of bonds.

The euro is likely to suffer from the fact that the ECB will resume its net purchases of bonds. We have therefore lowered our year-end forecast for EURNZD from 1.7850 to 1.76 level.

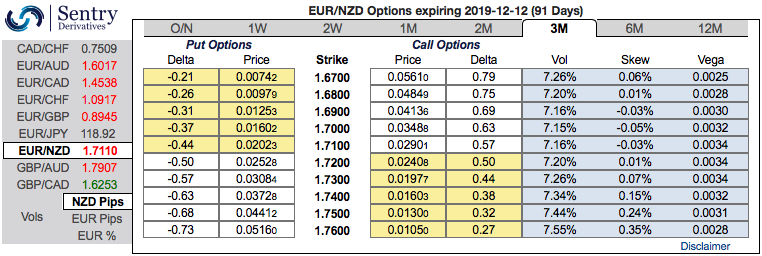

OTC outlook and Hedging Strategy:

Please be noted that the positively skewed IVs (implied volatilities) of 3m tenors signify the hedgers’ interests on both upside and downside risks (refer above nutshell). Bids for OTM calls and OTM put strikes up to 1.76 and 1.67 levels respectively are observed ahead of ECB monetary policy that is scheduled for today.

Contemplating all the above factors, we advocate 3m (1%) in the money delta call options and 2 lots of at the money put options of 1m tenors.

Thereby, in the money call option with a very strong delta will move in tandem with the underlying spot fx in the long term, while ATM Puts for the interim downswings.

Alternatively, we also advocate directional hedges as downside risks in the near terms are foreseen ahead of ECB’s monetary policy, initiate shorts in EURNZD futures contracts of near month expiries and simultaneously, longs in mid-month tenors with a view to arresting major uptrend. Courtesy: Sentrix & JPM