Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand

Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand  UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty

UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty  US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts

US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts  US Gas Market Poised for Supercycle: Bernstein Analysts

US Gas Market Poised for Supercycle: Bernstein Analysts  Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed

Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed  Wall Street Analysts Weigh in on Latest NFP Data

Wall Street Analysts Weigh in on Latest NFP Data  Bank of America Posts Strong Q4 2024 Results, Shares Rise

Bank of America Posts Strong Q4 2024 Results, Shares Rise  China’s Growth Faces Structural Challenges Amid Doubts Over Data

China’s Growth Faces Structural Challenges Amid Doubts Over Data  Moldova Criticizes Russia Amid Transdniestria Energy Crisis

Moldova Criticizes Russia Amid Transdniestria Energy Crisis  Energy Sector Outlook 2025: AI's Role and Market Dynamics

Energy Sector Outlook 2025: AI's Role and Market Dynamics  Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms

Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms  Global Markets React to Strong U.S. Jobs Data and Rising Yields

Global Markets React to Strong U.S. Jobs Data and Rising Yields  S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays

S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays  Urban studies: Doing research when every city is different

Urban studies: Doing research when every city is different  2025 Market Outlook: Key January Events to Watch

2025 Market Outlook: Key January Events to Watch  Stock Futures Dip as Investors Await Key Payrolls Data

Stock Futures Dip as Investors Await Key Payrolls Data  China's Refining Industry Faces Major Shakeup Amid Challenges

China's Refining Industry Faces Major Shakeup Amid Challenges

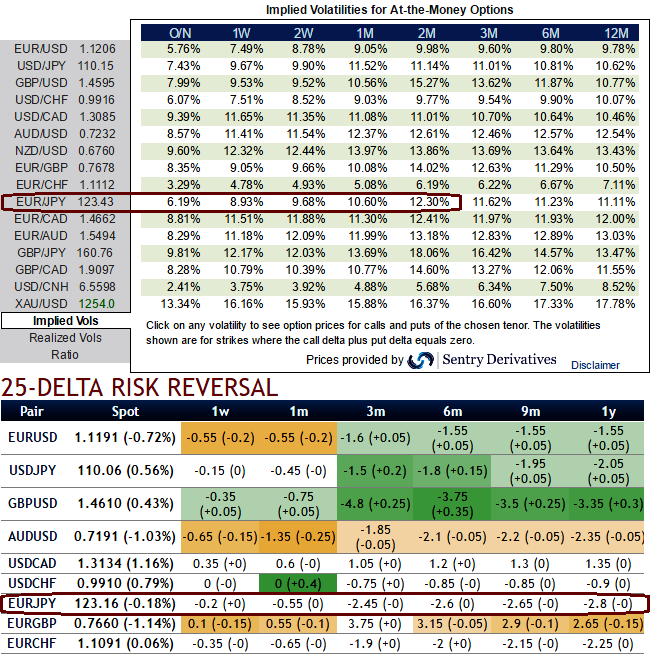

OTC Updates: The current implied volatility of ATM contracts is at 6.19% and little below 9% for 1w expiries but inching higher 12% for 2m tenors which means favourable atmosphere for option holders in OTC markets.

But as you can observe delta risk reversals are indicative of participants in this pair are more concerned about further slumps especially from next 3 months timeframe.

Rising negative flashes indicates active hedging sentiments for these downside risks but these risk reversals have neutral to slightly showing a sense of recoveries.

Well, that is where a shrewd option is likely to target, shrinking IVs with neutral to minor positive numbers renders the opportunities for short term option writers (compare 1w IVs at 6.19 with 1w delta RR).

25-delta risk reversal reveals the difference in volatility, and therefore price, between puts and calls on the most liquid out-of-the-money (OTM) options quoted on the OTC market, subsequently, the put are the expensive comparatively to the calls.

Acknowledging the gradual increase in the implied volatility of EURJPY but with higher negative risk reversals in long run is justifiable when you have to anticipate forwards rates and observe the spot curve of this pair (see IVs, RR nutshell, Sensitivities, and compare with spot prices).

Technically, the recent rallies have now tested and rejected resistance at 21DMA & 124.445 levels (daily charts), that’s where a “Shooting Star” pattern occurs, as a result, we see bears resuming again, the major downtrend has been slipping through falling wedge formation on monthly charts, current prices testing supports at baseline of falling wedge, the current prices remain well below EMAs despite attempts of bounces.

Major trend is declining trend, from last two years or so the pair has consistently evidenced price slumps more than 17%, and we could still foresee more downside potential ahead.

Hedging Positioning:

Pondering over above reasoning, one can still eye on loading up with fresh longs for long term hedging for downside risks, load up weights in longs comprising ATM instruments and ITM shorts in short term would optimize the strategy.

Hence, “Short 1W (1%) ITM put option, go long in 2 lots of 1M ATM +0.49 delta put options, thereby net delta should remain at around -0.66 and the strategy would be in theta advantage on both short and long side as we've chosen narrowed strikes as well expiries.”

We used narrowed expiries so as to suit the OTC market trends and to reduce the hedging cost. The quantum in above mentioned strategy is just for demonstration purpose only, one can load up weights according to the FX exposure in their portfolio.