UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data

UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data  2025 Market Outlook: Key January Events to Watch

2025 Market Outlook: Key January Events to Watch  US Gas Market Poised for Supercycle: Bernstein Analysts

US Gas Market Poised for Supercycle: Bernstein Analysts  Fed May Resume Rate Hikes: BofA Analysts Outline Key Scenarios

Fed May Resume Rate Hikes: BofA Analysts Outline Key Scenarios  China's Refining Industry Faces Major Shakeup Amid Challenges

China's Refining Industry Faces Major Shakeup Amid Challenges  Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes

Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes  Stock Futures Dip as Investors Await Key Payrolls Data

Stock Futures Dip as Investors Await Key Payrolls Data  World Cup technology: from ref cams to AI analysts, cutting-edge research is changing the game

World Cup technology: from ref cams to AI analysts, cutting-edge research is changing the game  US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts

US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts  With Iran and the US signing a peace deal, where does that leave Benjamin Netanyahu?

With Iran and the US signing a peace deal, where does that leave Benjamin Netanyahu?  Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand

Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand  Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure

Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure  Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms

Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms

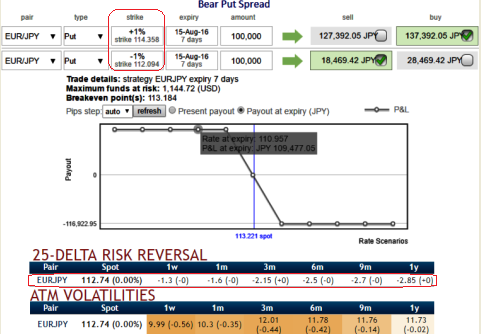

As the delta risk reversals have again shown in bearish interests as the progressive increase in negative numbers signify the traction for hedging sentiments for further downside risks in both short and long term.

Amid the apprehensions on perimeters of the policy arsenal at the BoJ and rising euro-centric risks, we recommend initiating short EURJPY positions for long-term hedging but by capitalizing on every short-term upswing, preferably via options during upcoming ECB meetings.

Until there is real domestically-generated inflation, it is hard to call EUR sustainably higher. Eventually, we think EUR recovers but it will be in a snail’s pace.

Well, in order to benefit from a favourable market move up to the higher strike:

As shown in the diagram for pay-off function of a debit put spread of EURJPY, below factors are indicative as to how it works at expiry, one of the following scenarios may occur:

1) Underlying trades below the lower strike then you sell the notional amount at the lower strike.

2) Underlying trades at or above the lower strike and below the higher strike, no transaction takes place on the settlement date. You could sell the notional amount at the prevailing spot rate (outside this structure).

3) Underlying trades at or above the higher strike, then you are obliged to sell the notional amount (multiplied by the leverage factor, if any) at the higher strike. Your profit potential is limited at the higher strike.