FxWirePro: GBP/AUD edges higher but bullish outlook persists

FxWirePro: GBP/AUD edges higher but bullish outlook persists  FxWirePro: GBP/NZD gaining momentum for a move towards 2.3100 level

FxWirePro: GBP/NZD gaining momentum for a move towards 2.3100 level  ETH Bounces as Shorts Cover, Yet ETF Bleed Warns $1,850 Resistance Won’t Break

ETH Bounces as Shorts Cover, Yet ETF Bleed Warns $1,850 Resistance Won’t Break  FxWirePro- Major Crypto levels and bias summary

FxWirePro- Major Crypto levels and bias summary  FxWirePro: EUR/AUD bullish outlook with scope to target 1.6550

FxWirePro: EUR/AUD bullish outlook with scope to target 1.6550  FxWirePro- Major Crypto levels and bias summary

FxWirePro- Major Crypto levels and bias summary  FxWirePro : AUD/USD drifts lower, could be on verge of bigger drop

FxWirePro : AUD/USD drifts lower, could be on verge of bigger drop  FxWirePro: USD/CAD uptrend loses steam, remains on bullish path

FxWirePro: USD/CAD uptrend loses steam, remains on bullish path  FxWirePro: AUD/USD drifts lower, uninspired by jobs beat

FxWirePro: AUD/USD drifts lower, uninspired by jobs beat  FxWirePro: USD/ZAR slips as dollar weakens after PCE inflation data

FxWirePro: USD/ZAR slips as dollar weakens after PCE inflation data  AUDJPY Bears Take a Breather at 111.50, But ‘Sell on Rallies’ Still Eyes 110

AUDJPY Bears Take a Breather at 111.50, But ‘Sell on Rallies’ Still Eyes 110  FxWirePro- Major Pair levels and bias summary

FxWirePro- Major Pair levels and bias summary  FxWirePro : GBP/NZD uptrend loses steam, remains on bullish path

FxWirePro : GBP/NZD uptrend loses steam, remains on bullish path  FxWirePro- Woodies pivot (Major)

FxWirePro- Woodies pivot (Major)  FxWirePro: USD/CAD hits 14-month high , Scope for further upside

FxWirePro: USD/CAD hits 14-month high , Scope for further upside  FxWirePro: USD/ZAR remains buoyant, looks to extend gains

FxWirePro: USD/ZAR remains buoyant, looks to extend gains

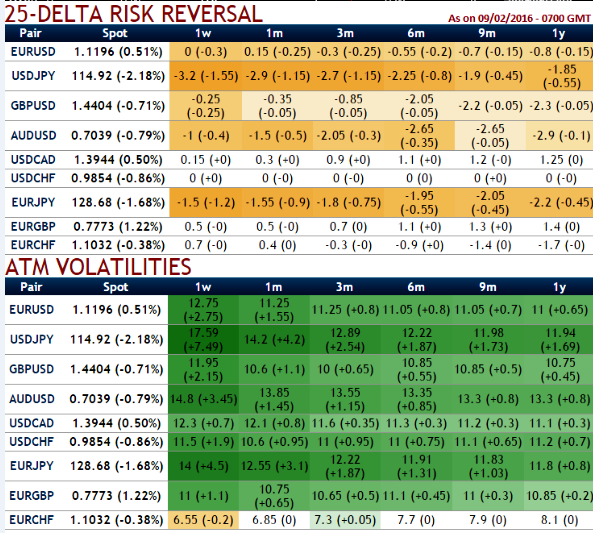

EUR/GBP forward volatility is cheaper (for next 3 months expiries) because EUR risk (shifting the entire curve higher) somewhat offsets future GBP risk (causing the steepness of both GBP curves).

However, EUR risk is more imminent than GBP risk and should be concentrated in the front end, consistent with the inverted EUR/USD curve (the EUR/USD 6M forward premium is negative).

Options are also discounting a large EUR risk on a forward basis (European fallout of a Brexit), reducing the EUR/GBP forward premium.

Buy EUR/GBP 1Y delta call strike at 0.80, Sell 1M call strike at 0.85 Indicative offer: 0.65% (spot ref: 0.7750)

Risks: Since risk reversals are pointing higher and favoring euro's gains, early EUR/GBP appreciation. The risk of the calendar call structure is limited to the premium paid up to seven months (expiry of the short option).

Beyond this date, investors could face unlimited topside risk if EUR/GBP trades above the 0.80 strike at the 7M intermediate expiry but below it at the 1Y final expiry.

In that event, the long option would be out of the money, realizing the loss supported four months earlier on the short option.

GBP/USD would fall more than EUR/GBP would rise in a Brexit scenario. However, this does not imply that the optimal hedging solution is expressed in cable. We have devised a directional forward hedge that takes advantage of the complacency in EUR/GBP forward volatility and skew.

The area of profitability in seven months is between 0.75 and 0.87, and if EUR/GBP is below 0.80 at end-June, investors would be left long a 5M call paid at a lower premium ahead of the referendum, with full topside and vega exposure.

- News

- Economy

- Central Banks

- Investing

- Research

- Roundups

- Digital Currency

- Insights

- Technical Analysis

- Technology

- Business

- Law

- Health

- Nature

- Fintech

- Science

- Topic

- Opinions

- ©Econometrics LLC . All Rights Reserved.

FxWirePro: EUR/GBP and GBP/USD vols look cheaper than EUR/USD in Brexit scenario

Wednesday, February 10, 2016 12:17 PM UTC

Editor's Picks

- Market Data

Most Popular