BOJ Rate Hike Expected to Boost Yen, Impact USD/JPY and Nikkei

BOJ Rate Hike Expected to Boost Yen, Impact USD/JPY and Nikkei  UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty

UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty  China Sets 1.25% Overnight Reverse Repo Rate Below Market Expectations

China Sets 1.25% Overnight Reverse Repo Rate Below Market Expectations  Michael Burry Shorts Tesla at $416 as AI and Semiconductor Bearish Bets Expand

Michael Burry Shorts Tesla at $416 as AI and Semiconductor Bearish Bets Expand  Urban studies: Doing research when every city is different

Urban studies: Doing research when every city is different  Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand

Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand  The government is ‘doubling down’ on its social media ban. But bigger penalties for platforms aren’t enough

The government is ‘doubling down’ on its social media ban. But bigger penalties for platforms aren’t enough  Japan Signals Preference for Low Interest Rates as BOJ Policy Debate Intensifies

Japan Signals Preference for Low Interest Rates as BOJ Policy Debate Intensifies  BoE Policymaker Alan Taylor Signals No Need for Interest Rate Hike Amid Iran War Inflation Risks

BoE Policymaker Alan Taylor Signals No Need for Interest Rate Hike Amid Iran War Inflation Risks  RBA Expected to Hold Interest Rates at 4.35% as Markets Watch AUD/USD and ASX 200

RBA Expected to Hold Interest Rates at 4.35% as Markets Watch AUD/USD and ASX 200  Central Banks Eye Gold, Reduce Dollar Exposure as AI Adoption Accelerates: OMFIF Survey

Central Banks Eye Gold, Reduce Dollar Exposure as AI Adoption Accelerates: OMFIF Survey  Buy the Dip: Gold Holds Strong at $3980, Targets $4150

Buy the Dip: Gold Holds Strong at $3980, Targets $4150

Sterling’s intraday drop, falling downbeat comments from lead EU negotiator Michel Barnier – who stated, “we are in deadlock” – highlights the sensitivity that the currency market displays to Brexit-related developments. The potential for a negotiation impasse was reinforced by sources attributed to UK officials (reported by Bloomberg) suggesting that the UK sees a “Brexit breakdown” if the EU refuses to compromise and progress to trade discussions.

Asymmetric uptick in G10 vols is more difficult to envision, since the mix of Fed repricing and tax reform optimism may draw a soft floor under the greenback for the time being even if this week’s upturn does not repeat, and coupled with the somewhat panicky unwinding of Euro (and other European FX) longs might leave macro investors less willing to spend option premium to play for EUR resurgence.

In this situation, if one had to pick one Euro bloc currency to buy vol in, our preferred pick would be GBP, especially on the crosses. We continue to believe that the abrupt shift in BoE policy and the attendant possibility of a policy mistake make sterling a fundamentally more uncertain currency than many others.

The range of spot outcomes on cable has now opened up from a previously narrow 1.28-1.30 band to a much wider 1.28 -1.36 (or higher) which ought to command a higher premium in implied vols than before. Yet GBP implied vols have retraced 3/4ths of the ramp up from earlier this month, and the realized vols are clocking recently at 1 vol above short dated implieds, hence this appears to be a case of underpriced fundamental uncertainty with supportive technicals for gamma ownership.

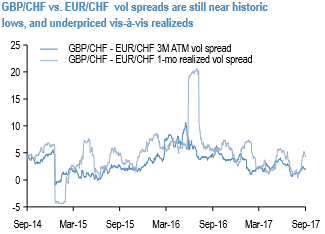

GBPCHF (GBP vs CHF implied correlation 40%, realized corrs 35%) in particular strikes as a useful long within the GBP-cross complex, we prefer financing it via shorts in EURCHF.

The GBPCHF – EURCHF vol spread has picked up from 15y lows but is still stuck near the bottom-end of a long-term range, the vol spread has a desirable tendency for one-sided eruptions in favor of a wider GBPCHF premium during market crashes, and enjoys a healthy positive carry at inception (2M ATM vol spread 1.9 mid, realized vol spread 4.0 on 1w and 4w look backs using hourly spot data; refer above chart).

From a tail risk standpoint, previous research shows that the RV is well-insulated to SNB shenanigans; we open a 2M ATM straddle spread this week. Courtesy: JPM

Currency Strength Index: FxWirePro's hourly GBP spot index is inching higher towards -119 levels (highly bearish), while hourly EUR spot index was at -97 (bearish) and CHF at 26 while (mildly bullish) articulating at 09:35 GMT. For more details on the index, please refer below weblink:

http://www.fxwirepro.com/currencyindex.

FxWirePro launches Absolute Return Managed Program. For more details, visit: