Denmark Central Bank Intervenes to Support Krone Peg Against Euro

Denmark Central Bank Intervenes to Support Krone Peg Against Euro  ECB Keeps July Rate Options Open Amid Iran War Energy Price Risks

ECB Keeps July Rate Options Open Amid Iran War Energy Price Risks  Central Banks Eye Gold, Reduce Dollar Exposure as AI Adoption Accelerates: OMFIF Survey

Central Banks Eye Gold, Reduce Dollar Exposure as AI Adoption Accelerates: OMFIF Survey  Japan Signals Surprise Yen Intervention Strategy as BOJ Hawkish Stance Puts FX Traders on Alert

Japan Signals Surprise Yen Intervention Strategy as BOJ Hawkish Stance Puts FX Traders on Alert  BoE Policymaker Alan Taylor Signals No Need for Interest Rate Hike Amid Iran War Inflation Risks

BoE Policymaker Alan Taylor Signals No Need for Interest Rate Hike Amid Iran War Inflation Risks  New Zealand Unemployment and Inflation Debate Intensifies Ahead of 2026 Election

New Zealand Unemployment and Inflation Debate Intensifies Ahead of 2026 Election  RBA Expected to Hold Interest Rates at 4.35% as Markets Watch AUD/USD and ASX 200

RBA Expected to Hold Interest Rates at 4.35% as Markets Watch AUD/USD and ASX 200  Japan Signals Preference for Low Interest Rates as BOJ Policy Debate Intensifies

Japan Signals Preference for Low Interest Rates as BOJ Policy Debate Intensifies  BOJ Rate Hike Expected to Boost Yen, Impact USD/JPY and Nikkei

BOJ Rate Hike Expected to Boost Yen, Impact USD/JPY and Nikkei  Taiwan Central Bank Likely to Keep Interest Rates Unchanged Through 2027

Taiwan Central Bank Likely to Keep Interest Rates Unchanged Through 2027  China Sets 1.25% Overnight Reverse Repo Rate Below Market Expectations

China Sets 1.25% Overnight Reverse Repo Rate Below Market Expectations  Supreme Court Backs Lisa Cook, Defends Federal Reserve Independence Against Trump Firing Attempt

Supreme Court Backs Lisa Cook, Defends Federal Reserve Independence Against Trump Firing Attempt  BOJ Raises Interest Rates to 1% as Inflation Pressures Persist

BOJ Raises Interest Rates to 1% as Inflation Pressures Persist  Malaysia Central Bank Moves to Support Ringgit Amid Foreign Fund Outflows

Malaysia Central Bank Moves to Support Ringgit Amid Foreign Fund Outflows  Fed Chair Kevin Warsh Signals Policy Overhaul as Hawkish Rate Outlook Rattles Markets

Fed Chair Kevin Warsh Signals Policy Overhaul as Hawkish Rate Outlook Rattles Markets

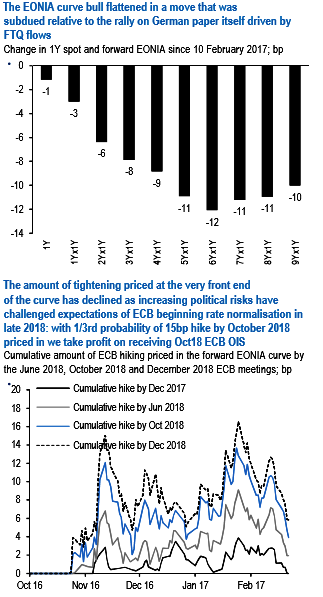

The EONIA curve bull flattened with a notable outperformance of post 5Y forwards (refer above diagram). The dynamic was different relative to the German curve, where the large outperformance of Schatz led to bull steepening of the German curve. Flight-to-quality flows on increasing concerns on French political risks were the main drivers.

The amount of tightening priced at the very front end of the curve has declined as increasing political risks have challenged expectations of ECB rate normalization in late 2018. We still believe that the ECB will increase policy rates 6M after the end of QE purchases which we expect at June 2018. With the market now pricing about 1/3rd probability of a 15 bp hike in the deposit rate by October 2018 (refer above diagram), we take profit on receiving Oct18 ECB OIS.

After the recent rally greens EONIA are now priced fully in line with our risk scenario of ECB starting to hike rates in late 2019 limiting the attractiveness of long positions in the sub 3Y sector (refer above diagram). Further out we are still biased for a steeper money market curve but we acknowledge that the political risks are going to limit the rate normalization priced in by the ECB, given the risk scenario of a Le Pen Presidency and potential EMU/EU referendum.

We prefer to hold steepening exposure in the money market curve via conditional structures. Specifically, we hold reds/blues weighted swap curve conditional steepener via 3M midcurve payers. The weighted curve continues to remain strongly directional and is currently trading too flat vs. yield levels (refer above diagram).

Two weeks ago we recommended conditional bull flattener to hedge against the risk of further FTQ driven rally combining the bull flattening view of the swap curve (1s/5s) with the bull widening view in Bobl swap spreads. Over the period the swap curve the bull flattened and Bobl swap spreads widened 8bp (refer above diagram). Thus we tactically take profit on 1Y swap/Jun17 Bobl conditional bull flattener. The richening of Bobl implied volatility has reduced the attractiveness of this conditional structure, with 3Mx1Y implied now priced at about 20-25% of Bobl implied volatility.