Stock Futures Dip as Investors Await Key Payrolls Data

Stock Futures Dip as Investors Await Key Payrolls Data  U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures

U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures  Bank of America Posts Strong Q4 2024 Results, Shares Rise

Bank of America Posts Strong Q4 2024 Results, Shares Rise  Energy Sector Outlook 2025: AI's Role and Market Dynamics

Energy Sector Outlook 2025: AI's Role and Market Dynamics  Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand

Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand  2025 Market Outlook: Key January Events to Watch

2025 Market Outlook: Key January Events to Watch  Goldman Sachs: US Dollar Likely to Stay Strong Despite Oil Price Retreat

Goldman Sachs: US Dollar Likely to Stay Strong Despite Oil Price Retreat  How AI prompting turned writerly description into an everyday skill

How AI prompting turned writerly description into an everyday skill  Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms

Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms  European Stocks Rally on Chinese Growth and Mining Merger Speculation

European Stocks Rally on Chinese Growth and Mining Merger Speculation  Geopolitical Shocks That Could Reshape Financial Markets in 2025

Geopolitical Shocks That Could Reshape Financial Markets in 2025  Gold's 365-Day EMA Streak Since Oct 2023 Faces Its First Real Test at $3,980 — Break or Bounce to $4,140?

Gold's 365-Day EMA Streak Since Oct 2023 Faces Its First Real Test at $3,980 — Break or Bounce to $4,140?  US Gas Market Poised for Supercycle: Bernstein Analysts

US Gas Market Poised for Supercycle: Bernstein Analysts  Today’s space race could turn fatal if we don’t agree on new rules

Today’s space race could turn fatal if we don’t agree on new rules

We know that bullish trend has again resumed and it likely to drag further to higher levels up to 1.0705 levels. Uptrend seems to be intensified especially after RBNZ stood pat in its yesterday’s monetary policy, leaving the OCR unchanged at 2.00%, which is in-line with the market expectations.

The MPS (monetary policy statement) acknowledged the economic developments since August and the NZ dollar has risen more than expected. After the central bank’s MPS, the market pricing for a November OCR cut has risen to around a 70% chance.

Technically, the flurry of bull streaks has been observed for this pair from last 6-7 consecutive days clearing major support levels in between this bullish rout. Current prices have spiked above DMAs to trade above 1.05 marks. So, any abrupt dips should be effectively utilized to build the ideal hedging strategy for the further upside risks.

1w ATM AUDNZD IVs are trading at 6.23% which is on a very lower side, while probabilistic numbers of put options signify the OTM strikes.

We know the rule that during higher IV circumstances, the market thinks the price has the potential for larger movement in either direction and lower IV implies that the OTC market anticipates the underlying spot price would not move much and so that it is beneficial for option writers.

As a result, one can think of reducing the hedging cost by deploying ITM shorts in call back spreads.

Hence, we recommend initiating more long call positions so as to hedge upside risks in this pair, call ratio back spread may probably attain the ideal hedging objective by reducing the hedging cost as well.

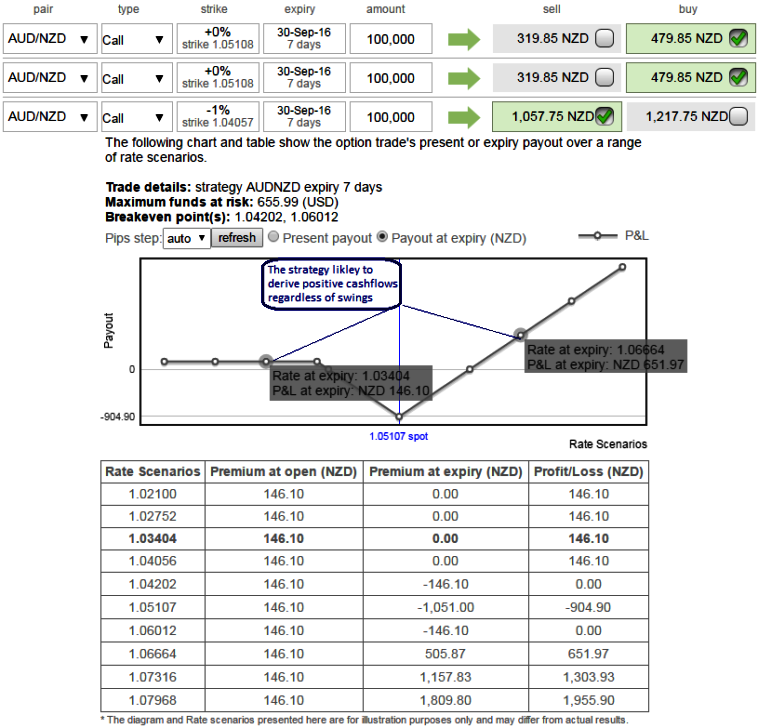

Hence, the strategy goes this way,

Long leg: 1M ATM +0.51 delta call, 1 lot of (1%) OTM +0.37 delta call and

Short leg: Simultaneously short 1 lot of deep OTM call (1%) of 2w expiry or with a comparatively shorter expiry in the ratio of 2:1.

The lower strike short calls seems little risky but because IV is reducing, the likelihood of options expiring in the money is very less and it finances the purchase of the greater number of long calls (ATM calls are overpriced, so we chose 1% OTM calls as well) and the position is entered for reduced cost.

As you can clearly observe that the irrespective of underlying spot rates, the above positions likely to derive positive cashflows.