Trump’s Iran Strategy: What Has Been Achieved After Three Months of Conflict?

Trump’s Iran Strategy: What Has Been Achieved After Three Months of Conflict?  Stock Futures Dip as Investors Await Key Payrolls Data

Stock Futures Dip as Investors Await Key Payrolls Data  US Gas Market Poised for Supercycle: Bernstein Analysts

US Gas Market Poised for Supercycle: Bernstein Analysts  Geopolitical Shocks That Could Reshape Financial Markets in 2025

Geopolitical Shocks That Could Reshape Financial Markets in 2025  Today’s space race could turn fatal if we don’t agree on new rules

Today’s space race could turn fatal if we don’t agree on new rules  J.P. Morgan Sees Potential Vestas Guidance Upgrade Amid Strong Wind Energy Demand

J.P. Morgan Sees Potential Vestas Guidance Upgrade Amid Strong Wind Energy Demand  World Cup technology: from ref cams to AI analysts, cutting-edge research is changing the game

World Cup technology: from ref cams to AI analysts, cutting-edge research is changing the game  Trump’s "Shock and Awe" Agenda: Executive Orders from Day One

Trump’s "Shock and Awe" Agenda: Executive Orders from Day One  China’s AI Manufacturing Boom Masks Weak Consumer Economy, Citi Says

China’s AI Manufacturing Boom Masks Weak Consumer Economy, Citi Says  Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close

Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close  Moldova Criticizes Russia Amid Transdniestria Energy Crisis

Moldova Criticizes Russia Amid Transdniestria Energy Crisis  UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data

UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data

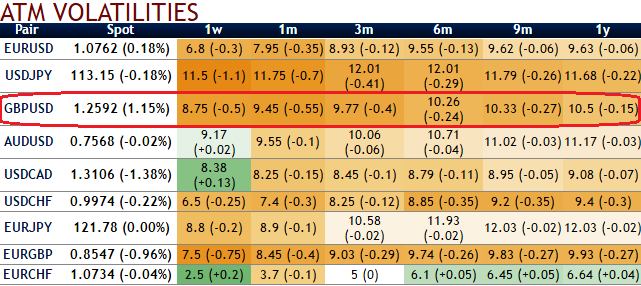

The view of a cable range and capped volatility directly suggests a Double No Touch (DNT) implementation. The risk is limited to the premium and the volatility profile is very interesting for the specific GBP risk.

Please be noted that the shrinking and lower implied volatility is observed in GBPUSD within G7 currency space despite BoE lined up for monetary policy on next Thursday: Refer IV nutshell, 1w implied volatility at 8.75%, against 11.5% and 6.8% for the USDJPY and EURUSD respectively), posing it comparatively economical to express a directional USD view through options.

This option is short vega so that it benefits from lower implied volatility. Vega is the sensitivity of an option’s value to a change in volatility. It is usually expressed as the change in premium value per 1% change in implied volatility.

This is intuitive due to the higher likelihood of the market ‘swinging’ in your favor. The options with a higher IV would usually be expensive. If IV increases and you are holding an option, this is good. Unfortunately, if you have sold an option, it is bad. A seller wants IV to fall so the premium falls. You should also note short-dated options are less sensitive to IV, while long-dated are more sensitive

It is also long volga, which means positive exposure to the volatility of volatility, and therefore to tail risk.

With a market horizon as long as six months and a decent volatility risk premium, the market implied probability of hitting the bounds of such a payoff will be sufficiently high to produce attractive leverage.

Cable in the middle of the 1.20-1.30 range is an attractive entry point. In current market conditions, setting the DNT (Double No Touch) bound at 1.19 and 1.30 produces leverage above 7 times.

After a surge due to GBP intrinsic risk, the EURGBP is going to be increasingly euro driven. EURGBP volatility is likely to rise as the EURUSD heads to parity, and then bounce as the ECB tapers purchases. At the same time, cable volatility should remain constrained, suggesting buying EURGBP volatility against GBPUSD.

Interestingly, the market is already pricing this volatility up to the 6m tenor, as the spread very recently turned negative, but the 1y spread is slower to adjust and will have to follow. Such a spread mitigates GBP risk, which is compensated in the two legs.

Since February 2016, the 1y spread has traded between flat and one volatility point and the Brexit headlines in June and October did not really shake it, conferring an attractive relative value feature.