Global Markets React to Strong U.S. Jobs Data and Rising Yields

Global Markets React to Strong U.S. Jobs Data and Rising Yields  Geopolitical Shocks That Could Reshape Financial Markets in 2025

Geopolitical Shocks That Could Reshape Financial Markets in 2025  US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts

US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts  Fed May Resume Rate Hikes: BofA Analysts Outline Key Scenarios

Fed May Resume Rate Hikes: BofA Analysts Outline Key Scenarios  S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays

S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays  Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms

Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms  Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data

Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data  European Stocks Rally on Chinese Growth and Mining Merger Speculation

European Stocks Rally on Chinese Growth and Mining Merger Speculation  Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes

Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes  Stock Futures Dip as Investors Await Key Payrolls Data

Stock Futures Dip as Investors Await Key Payrolls Data  U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?

U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?  U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures

U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures  Moldova Criticizes Russia Amid Transdniestria Energy Crisis

Moldova Criticizes Russia Amid Transdniestria Energy Crisis  Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand

Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand  China’s Growth Faces Structural Challenges Amid Doubts Over Data

China’s Growth Faces Structural Challenges Amid Doubts Over Data  Energy Sector Outlook 2025: AI's Role and Market Dynamics

Energy Sector Outlook 2025: AI's Role and Market Dynamics

The excessive yen skew premium Yen calls are in high demand for all crosses as the market is behaving in a risk-off way. As we wrote here and here, the yen probably met an inflexion point after months of strength.

A Trump victory would pressure the USDJPY and EURJPY towards the retest of 100 and 112.566 respectively but a break would not at all be to the BoJ’s taste, whereas the Fed is edging closer to a December hike, making a new rebound likely. Well, capitalizing the ongoing rallies to write the overpriced ITM puts would be a smarter approach while formulating hedging strategy through put ratio back spread.

Selling outright yen volatility or skew is not a reasonable trade given the imminent risk event, but selling the yen skew premium as a leg of a relative value trade appeals.

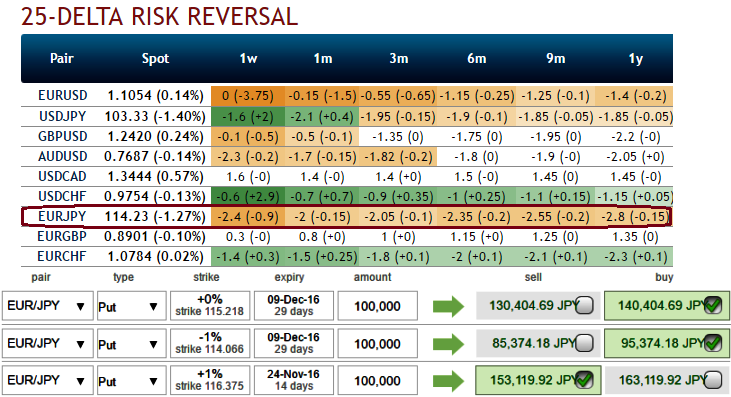

Stay short EURJPY rather than USDJPY skew, the EURJPY 3m skew is larger than the USDJPY skew (-2.1 vs -1.8), so that selling the former provides a higher premium.

Moreover, the EURJPY skew exceeding the USDJPY is not consistent in times of EUR topside volatility. On the contrary, euro bullishness should dampen the EURJPY skew, which is, therefore, an attractive sell.

The spread between EURJPY and EURUSD 3m risk reversals is now very elevated historically, as it is exceeding 1.5 vols (see above graphs).

It never happened between 2012 and 2015 and such a situation happened only very transitorily this year. We expect the gap between EURJPY and EURUSD skews to tighten.

As you can see delta risk reversals are indicative of participants in this pair are more concerned about further slumps especially in next 1month’s timeframe. Rising negative flashes indicate active hedging sentiments for these downside risks.

Acknowledging the gradual decrease in the implied volatility of EURJPY but with the higher negative risk reversals in long run is justifiable when you have to anticipate forwards rates and observe the spot curve of this pair (see IVs, RR nutshell, Sensitivities, and compare with spot prices).

The major declining trend is still under pressure, from the last two years or so the pair has consistently evidenced considerable price slumps from the last couple of months, and we could still foresee more downside potential ahead, hence, the long-term foreign traders are advised to safeguard their portfolios with this downside risks via below option strategy.

Hedging Positioning:

“Short 2w (1%) ITM put option, go long in 1 lot of long in 1m ATM -0.49 delta put options and another 1 lot of (1%) OTM -0.36 delta put of 1m25d tenor.” Using diagonal tenors would keep us hedging positions riskfree as well as reduces the cost of hedging to almost 50%.

The position is a spread with limited loss potential, but varying profit potential. The degree of profit relies on the strength and rapidity of price movement. The position uses long and short puts in a ratio, such as 2:1, to maximize returns.