Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed

Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed  Wall Street Analysts Weigh in on Latest NFP Data

Wall Street Analysts Weigh in on Latest NFP Data  U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?

U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?  Mexico's Undervalued Equity Market Offers Long-Term Investment Potential

Mexico's Undervalued Equity Market Offers Long-Term Investment Potential  Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand

Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand  US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts

US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts  Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes

Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes  Bank of America Posts Strong Q4 2024 Results, Shares Rise

Bank of America Posts Strong Q4 2024 Results, Shares Rise  U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures

U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures  S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays

S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays  European Stocks Rally on Chinese Growth and Mining Merger Speculation

European Stocks Rally on Chinese Growth and Mining Merger Speculation  Urban studies: Doing research when every city is different

Urban studies: Doing research when every city is different  Energy Sector Outlook 2025: AI's Role and Market Dynamics

Energy Sector Outlook 2025: AI's Role and Market Dynamics  2025 Market Outlook: Key January Events to Watch

2025 Market Outlook: Key January Events to Watch  Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data

Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data  US Gas Market Poised for Supercycle: Bernstein Analysts

US Gas Market Poised for Supercycle: Bernstein Analysts

Technically, this pair is bearish bias for the day as the last week’s bull swings seem to have given up the last week’s momentum when the pair tested resistance at 113.501 levels, while the prices on monthly chart consistently rejected through inverse saucer to push further downside. Price behaviour has been hovering at this level from 3-4 sessions (see 4H chart), while the prices on monthly chart consistently rejected at inverse saucer to push further downside.

On the other hand, 1m IV skews, risk reversals still indicate the bearish hedging sentiments in the FX OTC markets but IVs are equally conducive for both option holders as well as for writers.

From these risk reversal numbers, the hedging framework can individually be tailored, structured to mitigate the risk associated with the FX exposures. You can define:

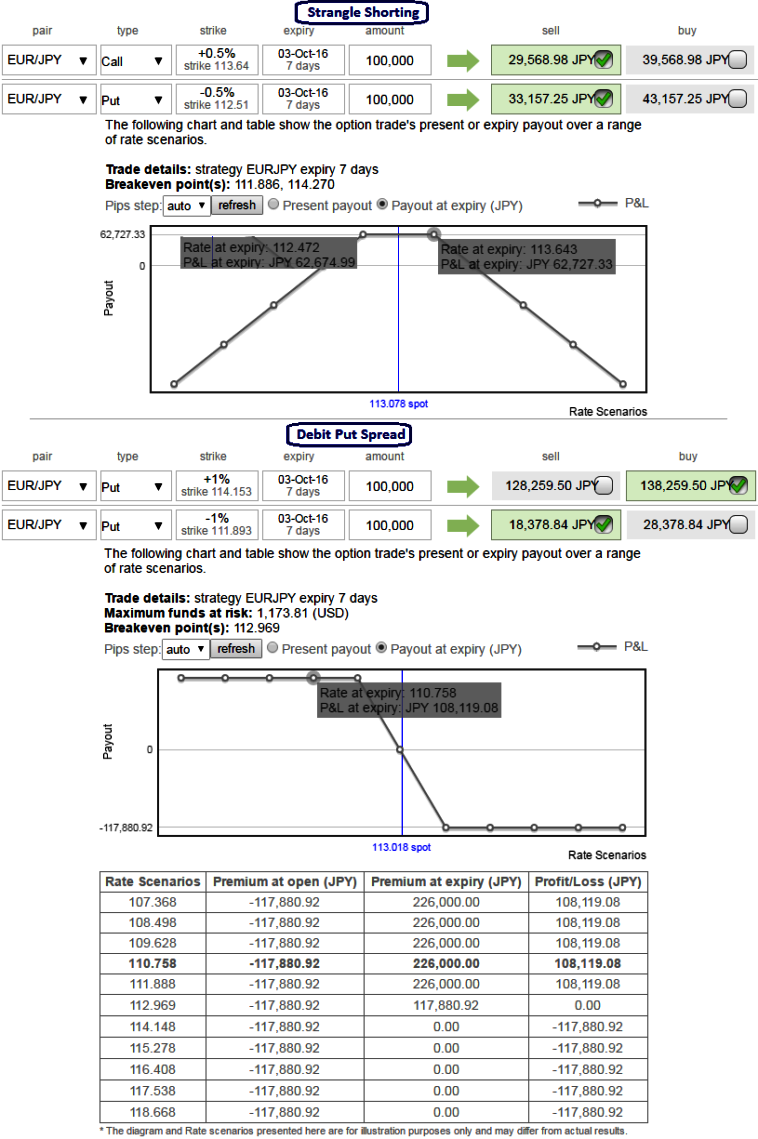

Option-trade recommendations:

- Writing a strangle

For those whose foresee non-directional that is existed in this pair from the last couple of months or so to prolong in reducing IV scenario, prefer to remain in the safe zone, we recommend shorting a straddle considering IV shrinks.

Thereby, one can benefit from certain returns by shorting both calls and puts.

Thus, short 7D (1% OTM striking) put and (1% OTM striking) call simultaneously of the same expiry (preferably the short term for maturity is desired).

The strategy is likely to derive the maximum returns as long as the EURJPY spot FX price on expiry is trading between 112.472 and 113.643 levels only as both the instruments have to wipe off worthless. So that the options trader gets to keep the entire initial credit taken as profit.

- Bear/Debit Put Spread (BPS):

As the risk appetite varies from different investors to different traders, we’ve customized our formulation of strategies for such varied circumstances.

On a hedging perspective, the foreign trader who are aggressively expecting slumps, debit put spreads are advocated as the selling indications are piling up on daily graph. So buying In-The-Money Puts and to reduce the cost of hedging by financing this long position, selling an Out-Of-The-Money put option is recommended.

We’ve shown how a typical debit put spread resembles like and its payoff structure, one can deploy such strategies if you are bearish on this pair but want to play it safe. The strategy is likely to generate positive cashflows as long as it keeps evidencing more slumps.