UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty

UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty  Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand

Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand  US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts

US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts  Stock Futures Dip as Investors Await Key Payrolls Data

Stock Futures Dip as Investors Await Key Payrolls Data  Moldova Criticizes Russia Amid Transdniestria Energy Crisis

Moldova Criticizes Russia Amid Transdniestria Energy Crisis  2025 Market Outlook: Key January Events to Watch

2025 Market Outlook: Key January Events to Watch  U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures

U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures  U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge

U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge  US Gas Market Poised for Supercycle: Bernstein Analysts

US Gas Market Poised for Supercycle: Bernstein Analysts  Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure

Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure  S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays

S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays  U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?

U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?  Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data

Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data  Wall Street Analysts Weigh in on Latest NFP Data

Wall Street Analysts Weigh in on Latest NFP Data  China’s Growth Faces Structural Challenges Amid Doubts Over Data

China’s Growth Faces Structural Challenges Amid Doubts Over Data  Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close

Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close  Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms

Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms

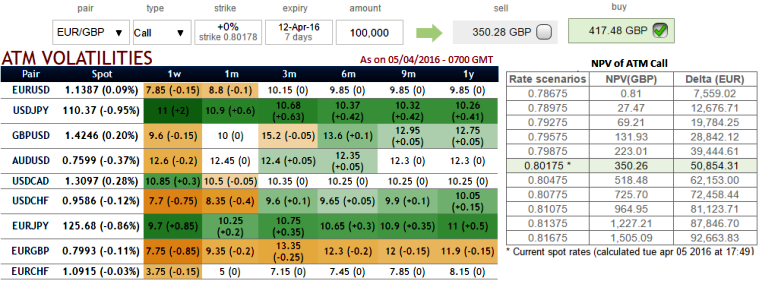

Let’s ponder a trader thought implied volatility of ATM EUR/GBP call option of 1W expiries indicate overpriced premiums (see diagram for premiums and its NPV).

Thus, it tends to short the volatility. Let's now suppose that we are writing an ATM call option with an amount of 100,000 EUR.

Currently, 1W ATM IVs of EURGBP and EURJPY are at 7.75% and 9.7% respectively.

Thereby, ATM premiums of EURGBP are trading 19.14% more than NPV.

The delta is positive 0.5 since this is an ATM EURGBP call option, the amount would be 50,000 EUR in spot outright.

To remove this potential risk taking place when the underlying market moves, we can buy 50,000 EUR against pounds in the spot market anticipating euro to go up and take the opposite position in EURJPY options as it was in EURGBP, because EURJPY is even more bearish with higher implied volatilities as you can probably observe from the IV and risk reversal nutshell.

This allows the delta neutral position. If prediction goes accurate then profit is certain by longs in call option and shots in EURJPY longs in puts with nil risk as the market moves around as long as you continue to update the Delta hedge.

But always keep in mind that adding long in an option in this case would mean that the returns are possible only when volatility spikes as anticipated.