U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures

U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures  Geopolitical Shocks That Could Reshape Financial Markets in 2025

Geopolitical Shocks That Could Reshape Financial Markets in 2025  Goldman Sachs: US Dollar Likely to Stay Strong Despite Oil Price Retreat

Goldman Sachs: US Dollar Likely to Stay Strong Despite Oil Price Retreat  China’s AI Manufacturing Boom Masks Weak Consumer Economy, Citi Says

China’s AI Manufacturing Boom Masks Weak Consumer Economy, Citi Says  European Stocks Rally on Chinese Growth and Mining Merger Speculation

European Stocks Rally on Chinese Growth and Mining Merger Speculation  Sell the Bounce": Gold Rally Stalls Near $4165 as Fed Hawks Slam the Door on Rate Cuts — Targets $4000/$3600

Sell the Bounce": Gold Rally Stalls Near $4165 as Fed Hawks Slam the Door on Rate Cuts — Targets $4000/$3600  US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts

US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts  World Cup technology: from ref cams to AI analysts, cutting-edge research is changing the game

World Cup technology: from ref cams to AI analysts, cutting-edge research is changing the game  UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty

UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty  China’s Growth Faces Structural Challenges Amid Doubts Over Data

China’s Growth Faces Structural Challenges Amid Doubts Over Data  US Gas Market Poised for Supercycle: Bernstein Analysts

US Gas Market Poised for Supercycle: Bernstein Analysts  Stock Futures Dip as Investors Await Key Payrolls Data

Stock Futures Dip as Investors Await Key Payrolls Data

USDCHF 3M3M FVAs: Owning USD/CHF vol appeals because it can benefit from the full gamut of risk triggers that can afflict all USD-vols, is a useful hedge overlay on a bullish Euro macro portfolio, and retains exposure to idiosyncratic CHF weakness of the kind seen recently, all without the threat of overt SNB management that can frustrate outsized sell-offs in EUR/CHF.

Geopolitical relief to pressure CHF. The North Korean missile test revived geopolitical tensions earlier this week, prompting market participants to bid the CHF and JPY (traditional safe-havens), mostly at the expense of the US dollar.

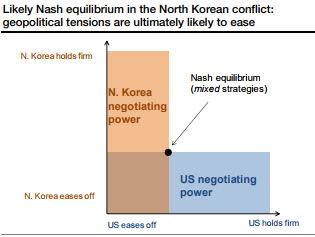

Through the prism of game theory, nuclear brinksmanship is a game of chicken (refer above graph), where the most likely equilibrium is that credible threats lead to a form of dissuasion. Assuming that the escalation between the US and North Korea will ease off, the Swiss Franc should sell off.

The technical analysts highlight that the USDCHF has bounced from the 0.9440 support and that breaking 0.9810 will trigger a greater recovery. The dollar hit a bottom.

Risk aversion pressured Treasury yields and the dollar, but US data releases surprised on the upside while the EURUSD appears to have overshot fundamental indicators, such as the real interest rate spread. After having tested the 1.2050 resistance, the EURUSD consolidation should extend further and benefit the USDCHF. Hence, optionality is recommended using fairly priced in calls.

Alternatively, the FVA format is motivated in part by the fact that USDCHF forward vols have severely lagged the surge in CHF-complex gamma, and partly by the mild inversion of the vol curve that ensures optically appealing flat slide/roll over time.

Admittedly some of the term structure shape is due to the forward starting 3M window covering the quiet holiday weeks of late December (3M3M = mid-November’17 to mid-February'18) that depresses 6M vol, but despite that, it may not be the worst idea to take delivery of and own USDCHF straddles through the first half of December that can reprise the above-average volatility of previous years around ECB and Fed meetings when tapering and rate hike decisions are expected to be announced. Courtesy: Societe Generale