European Stocks Rally on Chinese Growth and Mining Merger Speculation

European Stocks Rally on Chinese Growth and Mining Merger Speculation  Trump’s "Shock and Awe" Agenda: Executive Orders from Day One

Trump’s "Shock and Awe" Agenda: Executive Orders from Day One  Mexico's Undervalued Equity Market Offers Long-Term Investment Potential

Mexico's Undervalued Equity Market Offers Long-Term Investment Potential  BOJ Raises Interest Rates to 31-Year High, Signals Strong Focus on Inflation Risks

BOJ Raises Interest Rates to 31-Year High, Signals Strong Focus on Inflation Risks  New Zealand Unemployment and Inflation Debate Intensifies Ahead of 2026 Election

New Zealand Unemployment and Inflation Debate Intensifies Ahead of 2026 Election  Wall Street Analysts Weigh in on Latest NFP Data

Wall Street Analysts Weigh in on Latest NFP Data  Energy Sector Outlook 2025: AI's Role and Market Dynamics

Energy Sector Outlook 2025: AI's Role and Market Dynamics  Fed Chair Kevin Warsh Signals Policy Overhaul as Hawkish Rate Outlook Rattles Markets

Fed Chair Kevin Warsh Signals Policy Overhaul as Hawkish Rate Outlook Rattles Markets  Smartphones are helping filmmakers tell the stories the movie industry overlooks

Smartphones are helping filmmakers tell the stories the movie industry overlooks  US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts

US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts  Japan Signals Preference for Low Interest Rates as BOJ Policy Debate Intensifies

Japan Signals Preference for Low Interest Rates as BOJ Policy Debate Intensifies  ECB Keeps July Rate Options Open Amid Iran War Energy Price Risks

ECB Keeps July Rate Options Open Amid Iran War Energy Price Risks  Stock Futures Dip as Investors Await Key Payrolls Data

Stock Futures Dip as Investors Await Key Payrolls Data

As USDCNY breached a key support at 6.4772 levels recently, the market seems to be curious whether Chinese central bank would step up an effort to prevent its currency from appreciating too drastically.

China, with a mere 1.3% GDP surplus, has a FEER-consistent exchange rate that is 6.32 not that far from the current rate, really. Hence, PIIE agreement with Treasury Secretary Mnuchin’s conclusion that China is not manipulating its currency. In our opinion, CNY is not an outlier given the backdrop of broad USD weakness.

In this case, there is no emergency for the authorities to conduct a directional intervention. Over the foreseeable future, the PBoC would continue to anchor its currency to the currency basket.

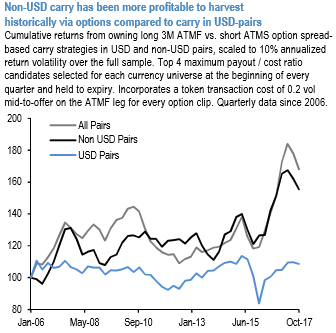

It is highlighted that elevated carry/vol ratios near multi-year highs represented the single most noteworthy thematic dislocation in FX options. This is a result of rising interest rates intersecting with über-depressed financial market volatility and enables earning the leveraged carry in an upbeat global growth environment with low option premium spend and defined maximum loss.

The pro-risk sleeve of our options portfolio is accordingly composed of ATMF vs. ATMS call spreads in two EM currency pairs, EURCNH and EURRUB; the former because of its loose correlation to the CNY TWI that is expected to remain stable in coming months, and the latter as a play on oil price strength with additional macro support from a positive current account.

Both pairs have been chosen to dodge outright exposure to the broad dollar, which has been in line with the anticipation of moderate USD strength through 1Q’18 at the time of writing, and is also the historically more profitable approach to carry trading – 1st chart illustrates a selection of the best four carry/vol currency pairs bought in ATMF/ATMS option spread format and held-to-expiry fared considerably better for the non-USD currencies than in USD pairs over the past decade.

Stability in EURCNH and EURRUB spot last month fully justifies their selection as pure carry candidates, though in hindsight, swifter delta gains would have resulted from simply owning USD puts. At the current market, the best value within the option-based carry universe resides in TWD/INR, EURTRY, and EURCNH (refer 2nd chart). Courtesy: JPM