Moldova Criticizes Russia Amid Transdniestria Energy Crisis

Moldova Criticizes Russia Amid Transdniestria Energy Crisis  Goldman Sachs: US Dollar Likely to Stay Strong Despite Oil Price Retreat

Goldman Sachs: US Dollar Likely to Stay Strong Despite Oil Price Retreat  How AI prompting turned writerly description into an everyday skill

How AI prompting turned writerly description into an everyday skill  2025 Market Outlook: Key January Events to Watch

2025 Market Outlook: Key January Events to Watch  Trump’s Iran Strategy: What Has Been Achieved After Three Months of Conflict?

Trump’s Iran Strategy: What Has Been Achieved After Three Months of Conflict?  US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts

US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts  UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty

UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty  Mexico's Undervalued Equity Market Offers Long-Term Investment Potential

Mexico's Undervalued Equity Market Offers Long-Term Investment Potential  Bank of America Posts Strong Q4 2024 Results, Shares Rise

Bank of America Posts Strong Q4 2024 Results, Shares Rise  Trump’s "Shock and Awe" Agenda: Executive Orders from Day One

Trump’s "Shock and Awe" Agenda: Executive Orders from Day One  Stock Futures Dip as Investors Await Key Payrolls Data

Stock Futures Dip as Investors Await Key Payrolls Data  Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed

Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed

Q1’2018 began with an accelerated unfolding of our anticipated baseline themes for 2018 – broad dollar weakness, policy repricing driving strength in non-dollar reserve and European currencies, and synchronized global cyclical strength supporting EM currencies.

But it is ending with a multitude of tail risks threatening to run-over the baseline outlook for 2Q and beyond. Trade tensions worsened significantly with Trump’s Section 301 announcement.

But the process of implementing tariffs on China will take around 45 days, and so we will remain on the uncertain cusp of potential broader trade-war well into 2Q.

This aggressive turn is also likely part of a broader shift in the Trump approach to policy and politics which may similarly translate into greater risks in two key areas: geopolitics and confrontation with the Mueller investigation. Through these headlines and other noise, the assumptions behind the baseline view (eventual ex-US policy normalization, constructive EM growth outlook, late-cycle US dynamics) has generally survived through 1Q.

Leveraged funds turned net buyers of USD for the first time in three weeks as trade tensions escalated and equities were sold. However, real asset managers sold USD amid market volatility.

Leveraged accounts were net buyers of JPY for 11 consecutive weeks, in line with the price action of USDJPY. Funds also bought EUR and GBP (helped by the EU-UK transition agreement reached the previous week).

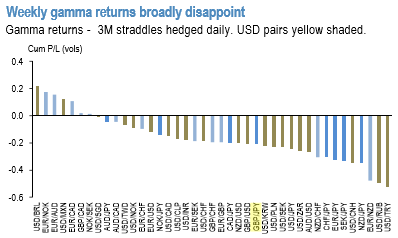

Usually, volatility produces return dispersion among large managers, while FX yields on gamma (refer 1st chart) withstood yet another week of agony as the busy calendar and panic from the US trade actions on the back of the Section 301 investigation report kept implieds supported but failed to revive realized vol (refer 2nd chart).

Moreover, April would consistently be the most FX vol downbeat month (refer above nutshell). That’s in part driven by vol supplying Japanese corporate hedging into the new fiscal year that directly impacts back tenor yen and yen x-vol ultimately spilling over into higher beta currencies.

The risk is that with the trade elephant still in the room, seasonal FX vol trends may be less notable this time around. Since the onset of the trade protectionism theme a few weeks ago and amid potential for a major left tail risk event we have turned defensive.

Our stance has been defensive bias and uphold onto longs cross-JPY vega in spread format (GBPJPY –USDJPY, BRLJPY – USDBRL), long EURUSD and EUR-cross (EURCAD) vol exposure and are short high dollar correlations (NZD vs. JPY) that should mean-revert lower if trade skirmishes intensify. Courtesy: JPM

FxWirePro launches Absolute Return Managed Program. For more details, visit: