U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures

U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures  2025 Market Outlook: Key January Events to Watch

2025 Market Outlook: Key January Events to Watch  Stock Futures Dip as Investors Await Key Payrolls Data

Stock Futures Dip as Investors Await Key Payrolls Data  Wall Street Analysts Weigh in on Latest NFP Data

Wall Street Analysts Weigh in on Latest NFP Data  European Stocks Rally on Chinese Growth and Mining Merger Speculation

European Stocks Rally on Chinese Growth and Mining Merger Speculation  Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms

Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms  Global Markets React to Strong U.S. Jobs Data and Rising Yields

Global Markets React to Strong U.S. Jobs Data and Rising Yields  China's Refining Industry Faces Major Shakeup Amid Challenges

China's Refining Industry Faces Major Shakeup Amid Challenges  S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays

S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays  Trump’s "Shock and Awe" Agenda: Executive Orders from Day One

Trump’s "Shock and Awe" Agenda: Executive Orders from Day One  U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?

U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?  US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts

US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts  US Gas Market Poised for Supercycle: Bernstein Analysts

US Gas Market Poised for Supercycle: Bernstein Analysts  Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data

Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data  Energy Sector Outlook 2025: AI's Role and Market Dynamics

Energy Sector Outlook 2025: AI's Role and Market Dynamics  Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes

Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes  UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data

UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data

The news of the additional US tariffs also resulted in EM currencies/equities crumbling overnight. Apart from the Chinese readings, Asian manufacturing PMIs came in mixed to weaker. Short-end EMFX vols are ‘waking up’ again, with Chinese equities slumping in early trade on Friday.

Overall, expect USD-Asia upside to persist, especially with regional currencies now lacking the buffer of net portfolio inflows. Asian (govie and IRS) yields meanwhile may be expected to take the cue from the global core curves and explore the downside once again, flushing out any ambiguity witnessed immediately after the FOMC.

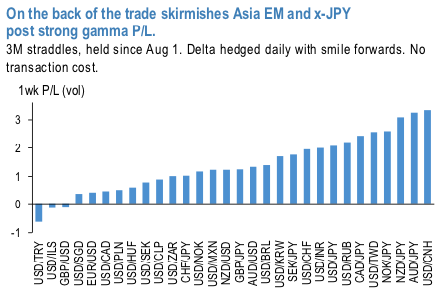

Spot gyrations generated strong gamma returns especially in Asia EM and x-JPY (refer 1st chart). 'How widespread and how impactful the trade escalation has been' is the best seen from the 1-week returns which are >90 percentile of YTD weekly returns for 26 out of 30 currencies in the Exhibit. We do not see a quick resolve and remain defensive though the current indications are that PBoC may want to bring back calm into FX.

The PBoC activity on clamping down the CNY day-to-day spot moves over the last few sessions shows that the central bank might be comfortable with the current level of FX weakness. CNY vols came off from the recent multi-year highs, and the 6M is now back to sub-6vol handle. The US-China trade developments remain very fluid and we are bound to see a few more adverse episodes.

Vol calendars: The front-back vol spread is another dislocation on the CNH vol surface. The CNH vol curve has inverted very sharply as front-end vols have risen alongside the CNY sell-off. The KRW and TWD vol surface show similar but less extreme setup. Under the PBoC spot management, CNY realized volatility is beginning to cool and the vol curve inversion should not be sustainable. That makes up for a risky but attractive opportunity for financing long vega bias by selling the front. It is well known that short front / long back tenor delta-hedged calendars have been systematically profitable in EMFX – and particularly so in Asia EM. The 2nd chart shows that short 3M / long 12M 25 delta puts vol calendar has fared well and displayed minimal drawdowns during May and the last week’s bout. Selling the front tenor downside instead of selling straddles provides a degree of safety as the short OTM CNH call option rapidly loses gamma as spot rallies. The JP Morgan’s "smart" model indicates TWD and CNH gamma to be the top-ranked sell candidate (refer 3rd chart).

Consider: Short 3M USDCNH 25 delta put @5.65 ch vs long 12M 25 delta put @5.4/5.675 indicative, vega neutral or short 3M USDTWD 25 delta put @5.1 ch vs long 12M 25 delta put @5.2/5.55 ch, vega neutral.

Cheap vega ownership: In anticipation of the vega tenors receiving more attention with the spot now under the watchful PBoC hand, we recommend using the favorable vol entry levels to add vega.

Moreover, pricing of the CNH skew offers an attractive setup to own cheap CNH vol exposure directly via 6M 25D USDCNH puts (delta-hedged), i.e. to own the weak (or the "wrong") side of the risk- reversal. The structure provides long vega exposure but at smaller decay costs. The choice of the delta strike (25D to 35D) reflects a trade-off between deriving adequate discount vis-à-vis ATM vols and gamma/vega exposure. Based on the historical P/L time series in 2ndchart the "wrong" side OTM vega has been an efficient proxy for the CNH ATM straddles during adverse episodes.

Consider: 6M or 9M USDCNH 25 delta puts @5.4/5.725 indicative for 6M and @ 5.375/5.675 indicative for 9M, delta hedged. Courtesy: JPM