CADJPY Outlook: Loonie Limps as Dismal Jobs Data Fuels BoC Rate Cut Bets

CADJPY Outlook: Loonie Limps as Dismal Jobs Data Fuels BoC Rate Cut Bets  FxWirePro- Major Pair levels and bias summary

FxWirePro- Major Pair levels and bias summary  FxWirePro: USD/CAD edges lower as oil rally strengthens Loonie

FxWirePro: USD/CAD edges lower as oil rally strengthens Loonie  FxWirePro: GBP/USD rises as UK political uncertainty fails to dent pound strength

FxWirePro: GBP/USD rises as UK political uncertainty fails to dent pound strength  FxWirePro: GBP/AUD edged higher, set to stay on back foot

FxWirePro: GBP/AUD edged higher, set to stay on back foot  FxWirePro: GBP/USD gaining momentum for a move towards 1.3700 level

FxWirePro: GBP/USD gaining momentum for a move towards 1.3700 level  Ethereum Technical Outlook: ETH Braces for Support as Bulls Eye the USD 2,200 Buy Zone

Ethereum Technical Outlook: ETH Braces for Support as Bulls Eye the USD 2,200 Buy Zone  Trump’s Hardline Stance Rattles Markets: BTC/USD Faces Volatility but Technicals Signal Strength

Trump’s Hardline Stance Rattles Markets: BTC/USD Faces Volatility but Technicals Signal Strength  Aussie Strength Prevails: AUD/JPY Targets Multi-Year Highs as Bullish Momentum Builds

Aussie Strength Prevails: AUD/JPY Targets Multi-Year Highs as Bullish Momentum Builds  FxWirePro: AUD/USD soften slightly but trend is still bullish

FxWirePro: AUD/USD soften slightly but trend is still bullish  FxWirePro: NZD/USD loses momentum but bullish setup remains

FxWirePro: NZD/USD loses momentum but bullish setup remains  FxWirePro: GBP/NZD downtrend loses steam, remains on bearish path

FxWirePro: GBP/NZD downtrend loses steam, remains on bearish path  GBPJPY Technical Check: Is the Dragon Running Out of Fire?

GBPJPY Technical Check: Is the Dragon Running Out of Fire?  Bitcoin Targets USD 90,000: Bullish Sentiment Solidifies as Realized Profits Surge

Bitcoin Targets USD 90,000: Bullish Sentiment Solidifies as Realized Profits Surge  FxWirePro: USD/CAD gains some momentum as weak Canadian jobs data weighs on loonie

FxWirePro: USD/CAD gains some momentum as weak Canadian jobs data weighs on loonie

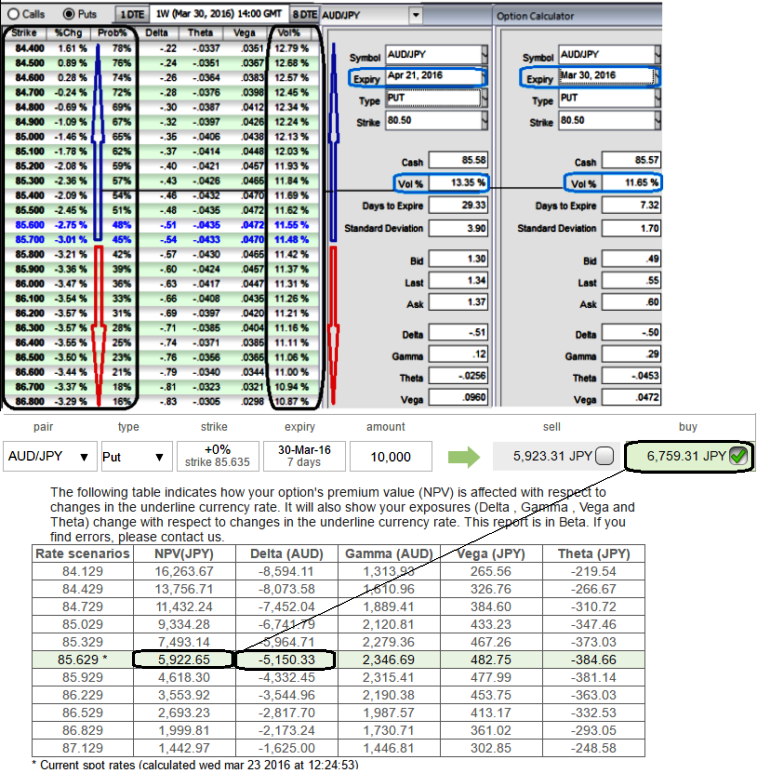

As shown in the diagram, please be noted that the Vega of OTM strikes are at the highest positive levels along with higher vols.

The premiums of ATM strikes are trading at around 14.13% more than NPV.

We know that the Vega is the sensitivity of an option’s value to a change in volatility (ATM vega is at JPY 482). It is usually expressed as the change in premium value per 1% change in implied volatility.

That means if the long option position has positive Vega and IVs spike or dip by every 1%, the option’s premium would also correspondingly increase or decrease by JPY 482.

Most importantly, 1W implied volatility is at the 11.65%, , these vols are spiking from 11.65% in 1w expiries to 13.35% in 1m expiries.

Options with a higher IV cost more. This is intuitive due to the higher likelihood of the market 'swinging' in your favour. If IV increases and you are holding an option, this is good. You should also note short-dated options are less sensitive to IV, while long-dated are more sensitive.

If you have to evaluate these vols and premiums with probabilistic figures in distinctive scenarios of OTM strikes, the options pricing seems reasonable, which means more likelihood of these puts expiring in the money.

Hence, we reckon the vega instruments are more conducive in bearish hedging.