RBA Minutes Signal Australia Central Bank Remains Ready to Raise Interest Rates if Inflation Persists

RBA Minutes Signal Australia Central Bank Remains Ready to Raise Interest Rates if Inflation Persists  Taiwan Central Bank Likely to Keep Interest Rates Unchanged Through 2027

Taiwan Central Bank Likely to Keep Interest Rates Unchanged Through 2027  BoE Policymaker Alan Taylor Signals No Need for Interest Rate Hike Amid Iran War Inflation Risks

BoE Policymaker Alan Taylor Signals No Need for Interest Rate Hike Amid Iran War Inflation Risks  BOJ Raises Interest Rates to 1% as Inflation Pressures Persist

BOJ Raises Interest Rates to 1% as Inflation Pressures Persist  Japan Signals Surprise Yen Intervention Strategy as BOJ Hawkish Stance Puts FX Traders on Alert

Japan Signals Surprise Yen Intervention Strategy as BOJ Hawkish Stance Puts FX Traders on Alert  New Zealand Unemployment and Inflation Debate Intensifies Ahead of 2026 Election

New Zealand Unemployment and Inflation Debate Intensifies Ahead of 2026 Election  BOJ Raises Interest Rates to 31-Year High, Signals Strong Focus on Inflation Risks

BOJ Raises Interest Rates to 31-Year High, Signals Strong Focus on Inflation Risks  Supreme Court Backs Lisa Cook, Defends Federal Reserve Independence Against Trump Firing Attempt

Supreme Court Backs Lisa Cook, Defends Federal Reserve Independence Against Trump Firing Attempt  China Sets 1.25% Overnight Reverse Repo Rate Below Market Expectations

China Sets 1.25% Overnight Reverse Repo Rate Below Market Expectations  Denmark Central Bank Intervenes to Support Krone Peg Against Euro

Denmark Central Bank Intervenes to Support Krone Peg Against Euro

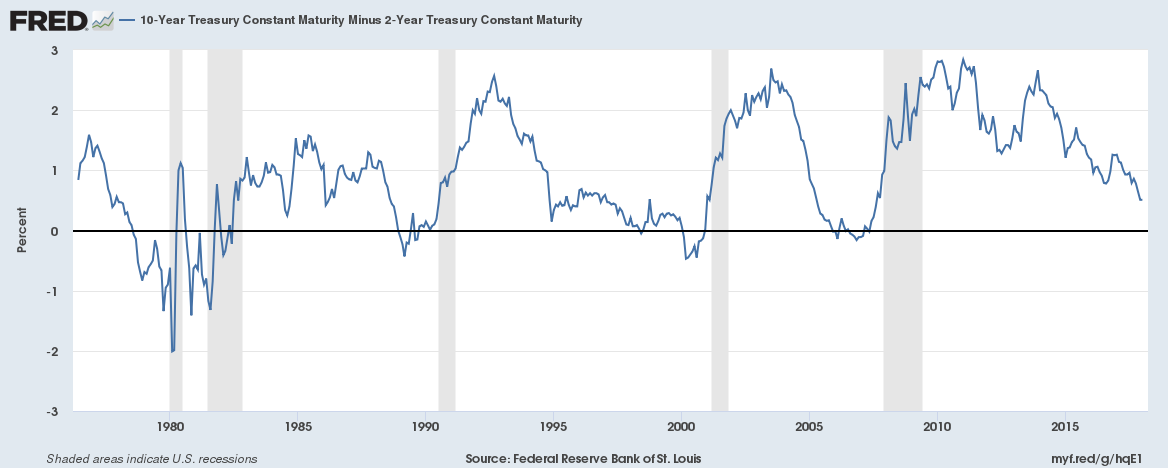

Since December 2015, the U.S. Federal Reserve has hiked interest rates five times; three times in 2017 alone, which has pushed the short-term interest rates higher. However, the increase of the U.S. Federal funds rate as well as the short-term interest rates was not met with a similar increase in the long-term rates, which increases the risk of yield curve inversion.

The above chart shows the difference between U.S. long-term rate (10-year) and short-term rate (2-year). The chart shows that the premium has fallen to just 51 basis points, which is the lowest level in more than a decade.

This is of high importance since the spread is widely accepted as one of the most reliable indicators of a coming recession. Every yield curve inversion was followed by a recession.

The U.S. Federal Reserve has announced plans for three more rate hikes in 2018 and if the long-term rates don’t start rising, such an increase would surely invert the yield curve.

Recently, Atlanta Fed President Raphael W. Bostic expressed similar worries.