FxWirePro: Daily Commodity Tracker - 21st March, 2022

FxWirePro: Daily Commodity Tracker - 21st March, 2022  Best Gold Stocks to Buy Now: AABB, GOLD, GDX

Best Gold Stocks to Buy Now: AABB, GOLD, GDX

Gilts have not been immune to the volatility in global markets with 10y rates moving in a 25bp range over the course of the week. Year to date, there have already been 58 days where the range in the Long Gilt Future has been greater than 0.5pt. This compares to just 43 days over all of 2014 and 57 days in 2013. There has been a sharp rise in realised volatility in longer-dated gilts but the front end of the curve has been relatively stable with rate expectations for the MPC now pushed out to Q4 16.

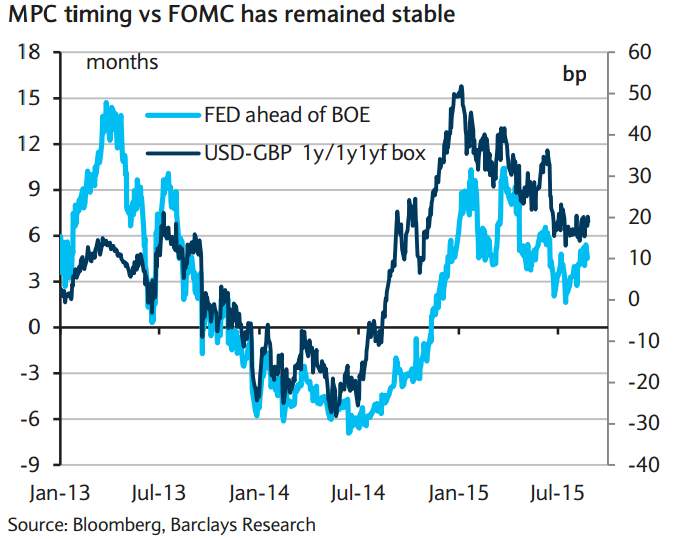

The relative timing of the first hike from the MPC versus the FOMC has remained reasonably steady at around five months (April vs September 2016, respectively). The market, while pushing out expectations for both central banks, has yet to materially alter the time lag between the two. While MPC members have insisted that they are not beholden to the FOMC, the market is unlikely to move back pricing the MPC moving ahead of the Fed as it did for much of 2014. On a relative basis, with GBP rates floored at 50bp compared to 15bp in the US, the GBP curve should be flatter than its USD equivalent. The box spread has richened from around 40bp to around 20bp. Given the "spot" spread of around 35bp in overnight rates, what would make the spread richen further? It is certainly possible that expectations for the FOMC are pushed out further but should that happen, expectations for earlier action from the MPC would also fall, maintaining the "timing" gap.

"We view it as unlikely that the market will return to pricing the MPC ahead of the FOMC as domestic activity data have not been strong enough and the latest downward move in commodity prices is likely to keep short-term inflation subdued", says Barclays.

One possible source of steepening could be that the MPC, faced with weakening inflation and falling expectations, might consider cutting the Bank rate. BOE Chief Economist Andy Haldane has noted that the outlook for the Bank rate in his view is balanced, although the Committee collectively sees the most likely move as higher.

- News

- Economy

- Central Banks

- Investing

- Research

- Roundups

- Digital Currency

- Insights

- Technical Analysis

- Technology

- Business

- Law

- Health

- Nature

- Fintech

- Science

- Topic

- Opinions

- ©Econometrics LLC . All Rights Reserved.

UK rates: Weekly review

Friday, August 28, 2015 1:49 AM UTC

Editor's Picks

- Market Data

Most Popular