Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed

Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed  Best Gold Stocks to Buy Now: AABB, GOLD, GDX

Best Gold Stocks to Buy Now: AABB, GOLD, GDX

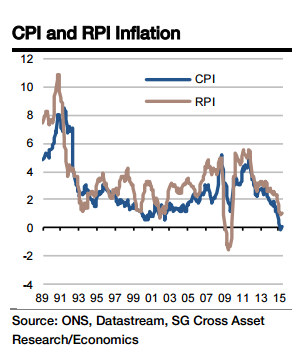

The June price data should show opposing influences cancelling each other out to leave the CPI inflation rate at 0.1% yoy. In May we were surprised to see food deflation ease by 1pp whilst food producer output price inflation was stable. Global food price deflation pressures is expected to continue to mount which should push down UK food prices as well so food deflation is expected to deepen again. Against that, petrol prices rose again in June and more strongly than a year earlier so making a positive contribution to inflation. Overall, the impact of commodity prices on the inflation rate should be zero. Core inflation should edge up.

"We predict that goods inflation will stay at -1.2% yoy as the downward pressure from the strong pound continues but services inflation should increase slightly from 2.3% to 2.4% as the tightening labour market starts to have an impact," says Societe Generale.

This should take core inflation from 0.9% to 1.0% yoy. The combination of stable commodity price inflation and a slightly higher core inflation rate should impart an upside risk to inflation. It should remain at 0.1% yoy with a risk of 0.2% yoy. RPI inflation should rise from 1.0% to 1.1% yoy.

- News

- Economy

- Central Banks

- Investing

- Research

- Roundups

- Digital Currency

- Insights

- Technical Analysis

- Technology

- Business

- Law

- Health

- Nature

- Fintech

- Science

- Topic

- Opinions

- ©Econometrics LLC . All Rights Reserved.

UK inflation stable at 0.1%

Monday, July 13, 2015 12:54 AM UTC

Editor's Picks

- Market Data

Most Popular