Ukraine’s drone strikes are having an impact on Russia — but Russian leaders remain committed to war

Ukraine’s drone strikes are having an impact on Russia — but Russian leaders remain committed to war  Same sparkle, different story: how lab-grown diamonds are transforming the market

Same sparkle, different story: how lab-grown diamonds are transforming the market  Gold Shines on Oil Relief: Buy Dips at $4160, Targeting $4305 as Bullish EMAs Dominate

Gold Shines on Oil Relief: Buy Dips at $4160, Targeting $4305 as Bullish EMAs Dominate  3 clinical-grade skincare creams you really shouldn’t buy online

3 clinical-grade skincare creams you really shouldn’t buy online  How an OpenAI safety test became a real-world cyberattack on the Hugging Face platform

How an OpenAI safety test became a real-world cyberattack on the Hugging Face platform  World game at war: why some European nations have threatened a World Cup boycott

World game at war: why some European nations have threatened a World Cup boycott

People's Bank of China (PBoC) last week devalued Yuan/Renminbi for three consecutive days. Offshore Renminbi fell from 6.2 against Dollar to trade as low as 6.59. However hovering close to 6.44 as of now against Dollar (USD/CNH).

While People's bank of China tried to assure market that it had been a controlled devaluation reflecting US monetary policy of rate hike, in reality it was a move of desperation.

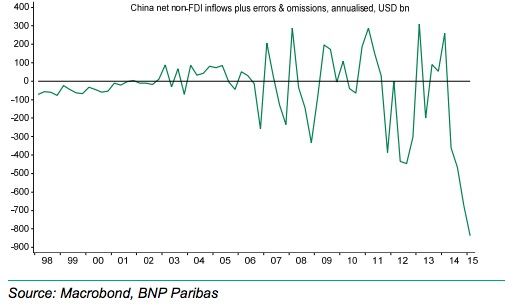

China experienced this year sharp fall of FX reserve in spite large current account surplus and positive foreign direct investment flow, suggesting rapid outflow of hot money (portfolio inflows/non-FDI flows).

The above chart from BNP Paribas, shows their estimate of hot money outflow in 2015, which according to BNP reached $209.5 billion for first quarter or at an annualized rate of $838 billion or 9.25% of GDP.

If this is true, PBoC was defending a very costly de-facto peg around 6.2 for several months had little choice but to devalue and release some of the pressure on Yuan.

PBoC's devaluation even if removes some of the pressure on Yuan it is unlikely to reverse the course of outflow of money from Chinese economy and probability stands high that it will get worse from here if devaluation spiral sets in.

In our view, PBoC is likely to have extremely difficult time, at one hand managing the Yuan de facto peg (now around 6.4), prevent tightening of the domestic monetary condition (Shibor is already on the rise) and discourage over risk taking and subprime lending.

Further devaluation, controlled or not seems very much likely.