DOJ Ends Probe Into Fed Chair Jerome Powell, Boosting Kevin Warsh Confirmation Prospects

DOJ Ends Probe Into Fed Chair Jerome Powell, Boosting Kevin Warsh Confirmation Prospects  Paraguay Holds Interest Rate at 5.5% as Inflation Remains Stable Amid Global Uncertainty

Paraguay Holds Interest Rate at 5.5% as Inflation Remains Stable Amid Global Uncertainty  Bank of Korea Signals Potential Interest Rate Hikes as Inflation Remains Elevated

Bank of Korea Signals Potential Interest Rate Hikes as Inflation Remains Elevated  Eurozone Recession Risks Rise as Middle East Conflict Threatens Growth, ECB Official Warns

Eurozone Recession Risks Rise as Middle East Conflict Threatens Growth, ECB Official Warns  RBA's Hauser Flags Uncertainty on Rate Settings Amid Iran War Economic Risks

RBA's Hauser Flags Uncertainty on Rate Settings Amid Iran War Economic Risks  Fed’s Goolsbee Warns Inflation Remains Elevated, Signals Caution on Rate Cuts

Fed’s Goolsbee Warns Inflation Remains Elevated, Signals Caution on Rate Cuts  Singapore Tightens Monetary Policy Amid Middle East War Inflation Risks

Singapore Tightens Monetary Policy Amid Middle East War Inflation Risks  South Korea Central Bank Signals Cautious Policy Amid Inflation and Middle East Tensions

South Korea Central Bank Signals Cautious Policy Amid Inflation and Middle East Tensions

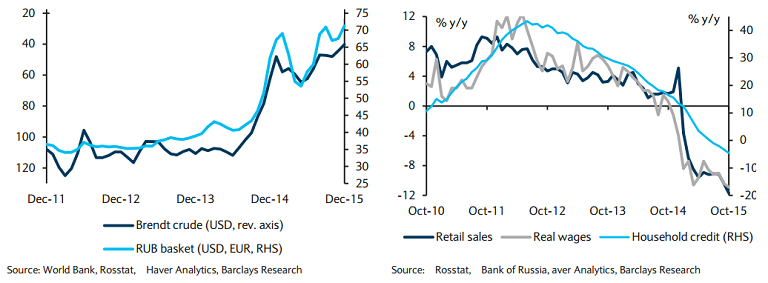

On 11 December 2015, the Bank of Russia decided to keep the key rate at 11.00 percent per annum, in recognition of growing inflation risks, but the risks of economic cooling remain. The bank estimates annual pace of consumer price growth in the end of 2016 to be about 6%, on the way to reach the target of 4% in 2017. Weakness in oil prices and the subsequent sell off of the RUB will help keep inflation subdued on base effects and thereby facilitate rate cuts beginning either at the next meeting at end-January or in mid-March. Real wages and retail sales will continue to declines in the November, while base effects and RUB weakness will likely help industrial production and real investment.

In Hungary, the NBH MPC meeting is due Tuesday, 15 December. The central bank, which has lowered interest rates to a record low and launched unconventional measures to fuel lending and growth, stands ready to employ more such unconventional means to stimulate the economy. The central bank could fine-tune its monetary easing toolkit in December, but expectations are for main interest rate to be kept hold at a record low 1.35 percent on Tuesday.

Hungary's headline CPI data for November came in at 0.5% y/y, slightly below expectations of 0.7%, while core inflation remained stable. But industrial production output, a leading indicator of real GDP, came in significantly stronger at 12.7% in the year to October, leading to the biggest October forecast surprise in this series since 2001.

"As a result of this positive news in the economy and the NBH's preference to loosen monetary conditions with more QE rather than cutting interest rates, we expect the NBH to remain on hold at 1.35% next week. We also expect Czech to remain on hold at 0.05% this week and to retain its exchange rate cap", says Barclays in a research note.

In the Czech Republic, November inflation disappointed, declining to 0.1% y/y from 0.2% in October, missing CNB expectations. With inflation well below the 1-3% target, the CNB is widely expected to keep its FX policy in place until at least H2 16, with the possibility of extension.

Poland's Monetary Policy Council kept the benchmark rate on hold at 1.50 percent earlier this month and ruled out a further cut to record low rates at the next policy meeting in January, saying economic growth was expected to accelerate next year. It will be interesting to watch Poland's release of the monthly external balance data tis week, along with the industrial production and retail sales figures. Expectations are for October current account and trade balances to come in at -€0.3bn and -€0.5bn, respectively.

- News

- Economy

- Central Banks

- Investing

- Research

- Roundups

- Digital Currency

- Insights

- Technical Analysis

- Technology

- Business

- Law

- Health

- Nature

- Fintech

- Science

- Topic

- Opinions

- ©Econometrics LLC . All Rights Reserved.

Low CEE inflation supports accommodative monetary policy

Monday, December 14, 2015 11:44 AM UTC

Editor's Picks

- Market Data

Most Popular