FxWirePro: Daily Commodity Tracker - 21st March, 2022

FxWirePro: Daily Commodity Tracker - 21st March, 2022

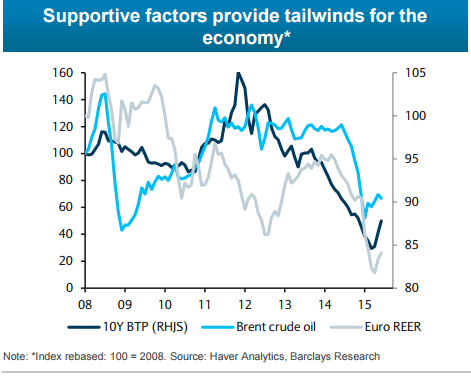

Barclays notes:

The Italian economy continues to benefit from tailwinds consistent with GDP expanding 0.8% this year and 1.4% next year. Risks are broadly balanced, we think, but should the situation in Greece precipitate, private sector confidence may retrench from current levels. Consumer and business confidence data suggest the pace of GDP expansion is likely to remain similar to Q1 (+0.3% q/q).

Private consumption should continue to benefit from low inflation, improving labour market and lending conditions and maintenance of the current neutral fiscal policy stance. Meanwhile, exports are expected to resume, fuelled by a weak euro and strengthening of global demand, including from the US economy (which absorbs about 20% of Italian exports outside the EU).

The latest set of labour market data shows the reform approved by the government at the beginning of March has already started to produce positive effects. The unemployment rate was unchanged at 12.4% (Feb-May), but open-ended labour contracts have increased significantly; the number of fixed-term contract activations eased. We continue to think that the government is likely to stay put on structural reforms, at least on those which are receiving a parliament reading (Senate, the judiciary and the public administration).

However, a weak result in local elections may weigh on the implementation of new reforms despite still relatively strong popularity of the government. Dissidents within the PD party may decide to take a more radical approach on the remaining reforms, possibly slowing the speed of reform

- News

- Economy

- Central Banks

- Investing

- Research

- Roundups

- Digital Currency

- Insights

- Technical Analysis

- Technology

- Business

- Law

- Health

- Nature

- Fintech

- Science

- Topic

- Opinions

- ©Econometrics LLC . All Rights Reserved.

Italy's economy on track, politics perhaps less so

Monday, July 27, 2015 8:37 PM UTC

Editor's Picks

- Market Data

Most Popular