UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty

UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty  Urban studies: Doing research when every city is different

Urban studies: Doing research when every city is different  JPMorgan Lifts Gold Price Forecast to $6,300 by End-2026 on Strong Central Bank and Investor Demand

JPMorgan Lifts Gold Price Forecast to $6,300 by End-2026 on Strong Central Bank and Investor Demand  Nasdaq Proposes Fast-Track Rule to Accelerate Index Inclusion for Major New Listings

Nasdaq Proposes Fast-Track Rule to Accelerate Index Inclusion for Major New Listings  Trump’s "Shock and Awe" Agenda: Executive Orders from Day One

Trump’s "Shock and Awe" Agenda: Executive Orders from Day One  Elon Musk’s Empire: SpaceX, Tesla, and xAI Merger Talks Spark Investor Debate

Elon Musk’s Empire: SpaceX, Tesla, and xAI Merger Talks Spark Investor Debate  China's Refining Industry Faces Major Shakeup Amid Challenges

China's Refining Industry Faces Major Shakeup Amid Challenges  Moldova Criticizes Russia Amid Transdniestria Energy Crisis

Moldova Criticizes Russia Amid Transdniestria Energy Crisis  US Gas Market Poised for Supercycle: Bernstein Analysts

US Gas Market Poised for Supercycle: Bernstein Analysts  European Stocks Rally on Chinese Growth and Mining Merger Speculation

European Stocks Rally on Chinese Growth and Mining Merger Speculation

The euro area corporates are in a good position to expand, the corporates in this geography have become net savers and low-interest costs, lower dividend payouts, lower CapEx explains the shift.

Corporates’ capacity to accelerate CapEx looks good.

A couple of months ago, we still expected the Euro area to grow at only a modestly above-trend pace this year. However, business and consumer sentiment have improved sharply, with the composite PMI signaling 3% growth in March. This prompted us to raise our 2017 growth forecast to 2.2% Q4.

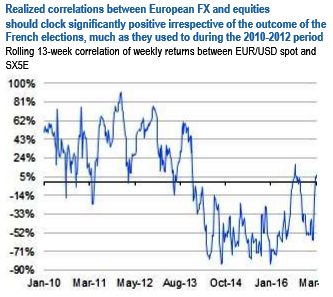

European FX vs. equity implied correlations currently trade in the 0 -20% range in 6M –1Y expiries, which might be fair relative to current realized correlations but ought to reprice higher in coming months if a concerted European asset rally reverts corrs back to average levels of the 2010-2012 period (refer above chart).

Investors have already started to take advantage of this dislocation and forced short-dated (<3M) EURUSD vs. SX5E correlations up to +25%, but there is still room for the move to play out in longer tenors.

EURUSD > 2% OTMS, SX5E > 5% OTMS: dual digitals costs 14.5% EUR indic. in 3M tenors (indiv. digis 43% and 26% respectively) and 18.5% EUR indic. in 1Y (indiv. digis 58% and 37% respectively).