Taiwan Central Bank Likely to Keep Interest Rates Unchanged Through 2027

Taiwan Central Bank Likely to Keep Interest Rates Unchanged Through 2027  Goldman Sachs Sees Fed Holding Interest Rates Steady Until 2027

Goldman Sachs Sees Fed Holding Interest Rates Steady Until 2027  BOJ Raises Interest Rates to 1% as Inflation Pressures Persist

BOJ Raises Interest Rates to 1% as Inflation Pressures Persist  South Korea Signals Possible Interest Rate Hike as Inflation Remains Elevated

South Korea Signals Possible Interest Rate Hike as Inflation Remains Elevated  Indonesia Plans Higher Asset Yields to Boost Rupiah and Restore Investor Confidence

Indonesia Plans Higher Asset Yields to Boost Rupiah and Restore Investor Confidence  ECB Set to Raise Interest Rates as Energy Shock Fuels Eurozone Inflation Concerns

ECB Set to Raise Interest Rates as Energy Shock Fuels Eurozone Inflation Concerns  Moldova Criticizes Russia Amid Transdniestria Energy Crisis

Moldova Criticizes Russia Amid Transdniestria Energy Crisis  Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data

Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data  Stock Futures Dip as Investors Await Key Payrolls Data

Stock Futures Dip as Investors Await Key Payrolls Data  Energy Sector Outlook 2025: AI's Role and Market Dynamics

Energy Sector Outlook 2025: AI's Role and Market Dynamics  Trump’s "Shock and Awe" Agenda: Executive Orders from Day One

Trump’s "Shock and Awe" Agenda: Executive Orders from Day One  BOJ Raises Interest Rates to 31-Year High, Signals Strong Focus on Inflation Risks

BOJ Raises Interest Rates to 31-Year High, Signals Strong Focus on Inflation Risks  RBI Hits Pause as Geopolitical Storm Clouds Gather

RBI Hits Pause as Geopolitical Storm Clouds Gather  Wall Street Analysts Weigh in on Latest NFP Data

Wall Street Analysts Weigh in on Latest NFP Data

The Russian rouble had weakened earlier in the spring, driven jointly by a collapse of the oil price and collapse of world economic activity. But when both these factors stabilised, the currency was able to rally noticeably and this, in fact, drove the central bank to accelerate the pace of its rate cuts. CBR used a large 100bp rate cut step in June before reverting to the smaller 25bp step in July. The outlook for the oil price has also become risky because of second wave fears. As a result of such developments, modest rouble underperformance is to be expected in the near-term. We could foresee USDRUB at 72.00 levels by Q3’2020 end, but forecast the exchange rate to trade at around the 70.00 mark by the year-end.

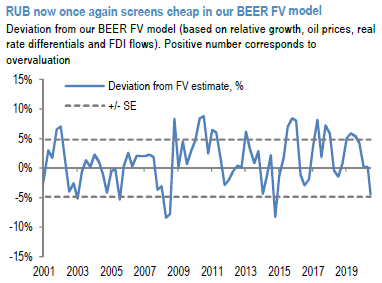

RUB should also benefit from an improved technical backdrop. Following the seasonal pressures, valuations once again appear attractive. We refer to JP Morgan’s BEER FV model that points to an undervaluation of around 3.4% (close to one standard deviation). This compares to an overvaluation of around 5%, when we first initiated tactical hedges (refer 1st chart). Ruble positioning remains relatively elevated in the latest J.P. Morgan client survey, with a score of +2.2 (ranking it the second largest EM FX OW in our survey).

However, we note higher frequency measures of spec positioning, as captured by IMM data, so positioning has been reduced over the past number of weeks (refer 2nd chart).

Accordingly, we saw this as an opportune time to take profits on USDRUB call spreads. With dividend pressure now abating and valuations once again screening cheap, positions have been squared-off and booked 0.86% of notional profit on tactical 1x1 USDRUB call spread (entry date: 30 June; spot ref of 71.74; exit spot ref of 74.01; option price at entry: 0.91%, option price at exit: 1.77%; profit: 0.86% of notional). We, now, maintain OW RUB in the GBI-EM model portfolio, expecting outperformance on an RV basis against fundamentally weaker high yielders in this region. Courtesy: JPM & Commerzbank