Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data

Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data  Brazil Cuts Selic Rate to 14% as Inflation Eases but Risks Persist

Brazil Cuts Selic Rate to 14% as Inflation Eases but Risks Persist  European Stocks Rally on Chinese Growth and Mining Merger Speculation

European Stocks Rally on Chinese Growth and Mining Merger Speculation  U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures

U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures  Urban studies: Doing research when every city is different

Urban studies: Doing research when every city is different  BOJ Rate Decision in Focus as Sticky Inflation, Weak Yen Shape USD/JPY and Nikkei Outlook

BOJ Rate Decision in Focus as Sticky Inflation, Weak Yen Shape USD/JPY and Nikkei Outlook  Mexico's Undervalued Equity Market Offers Long-Term Investment Potential

Mexico's Undervalued Equity Market Offers Long-Term Investment Potential  Trump’s "Shock and Awe" Agenda: Executive Orders from Day One

Trump’s "Shock and Awe" Agenda: Executive Orders from Day One  Singapore Central Bank’s Exchange Rate Policy Explained: Why MAS Uses the S$NEER Instead of Interest Rates

Singapore Central Bank’s Exchange Rate Policy Explained: Why MAS Uses the S$NEER Instead of Interest Rates  ECB Expected to Hold Rates as Middle East Tensions Keep September Hike in Focus

ECB Expected to Hold Rates as Middle East Tensions Keep September Hike in Focus  Global Markets React to Strong U.S. Jobs Data and Rising Yields

Global Markets React to Strong U.S. Jobs Data and Rising Yields  Energy Sector Outlook 2025: AI's Role and Market Dynamics

Energy Sector Outlook 2025: AI's Role and Market Dynamics

The BoJ maintains status quo in its monetary policy, focusing to soothing 10Y Treasury bond yield, the benchmark for long-term borrowing costs, at around zero pct and keep the overnight interest rate around -0.1%. and asset purchases program at ¥80 trillion.

The goal is to correct the excessively flat yield curve caused by its negative interest rate policy that took effect in February.

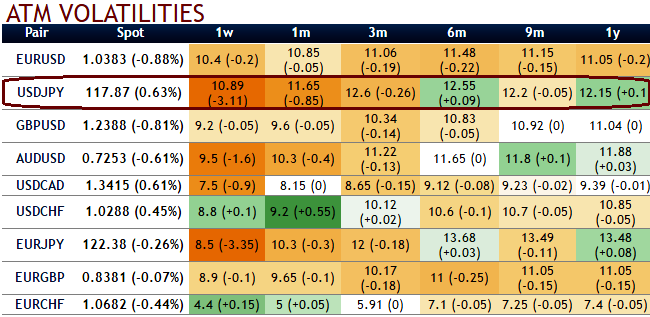

The recent fast spot upside lifted the 6m implied volatility to return to its highest level since 2013, which in itself is a reason to suspect mean-reversion will occur. It turns out that the relationship between spot and implied volatility suggests with more insistence that USDJPY.

Mounting global inflation, lifting US long yields, and persistent policy uncertainty have elected the dollar as the winner. The risk is for risk sentiment to change, thus the resilience of the risk mood bears watching because it is the key to the yen's continued weakness. Uncertainty is, however, unlikely to lift FX volatility further until the environment turns risk-off. Trump’s victory has so far not been conducive to such a shift.

On reduced central bank activity BoJ maintained unchanged monetary policy, which has committed to an overshooting commitment of achieving the 2% price stability target. The bank has shifted its primary tool for easing from quantity to the interest rate and, as the target is not a rigidly timed goal, the central bank is unlikely to implement additional easing. One of our key market themes was that the BoJ’s peg of long-term yields will transfer the suppressed rate volatility to the currency and equities.

You could probably understand the shrinking vols from the above IV nutshell and both RVs and IVs have constantly been making lower lows, this would demonstrate much about underlying USDJPY sentiments

Unlike NKY volatility, USDJPY volatility already has benefited from the volatility boost via an impressive topside acceleration. But now that US rates have picked up post the US election and following the Fed’s hike and adjustment higher of the dot plot, the yen depreciation should be more gradual. The market is due to take a breather which will dampen USDJPY realized volatility.