U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?

U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?  Supreme Court Backs Lisa Cook, Defends Federal Reserve Independence Against Trump Firing Attempt

Supreme Court Backs Lisa Cook, Defends Federal Reserve Independence Against Trump Firing Attempt  Geopolitical Shocks That Could Reshape Financial Markets in 2025

Geopolitical Shocks That Could Reshape Financial Markets in 2025  RBA Minutes Signal Australia Central Bank Remains Ready to Raise Interest Rates if Inflation Persists

RBA Minutes Signal Australia Central Bank Remains Ready to Raise Interest Rates if Inflation Persists  BOJ Raises Interest Rates to 1% as Inflation Pressures Persist

BOJ Raises Interest Rates to 1% as Inflation Pressures Persist  Global Markets React to Strong U.S. Jobs Data and Rising Yields

Global Markets React to Strong U.S. Jobs Data and Rising Yields  China’s Growth Faces Structural Challenges Amid Doubts Over Data

China’s Growth Faces Structural Challenges Amid Doubts Over Data  UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty

UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty  Trump’s "Shock and Awe" Agenda: Executive Orders from Day One

Trump’s "Shock and Awe" Agenda: Executive Orders from Day One  Japan Signals Surprise Yen Intervention Strategy as BOJ Hawkish Stance Puts FX Traders on Alert

Japan Signals Surprise Yen Intervention Strategy as BOJ Hawkish Stance Puts FX Traders on Alert  Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand

Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand  Indonesia Plans Higher Asset Yields to Boost Rupiah and Restore Investor Confidence

Indonesia Plans Higher Asset Yields to Boost Rupiah and Restore Investor Confidence  European Stocks Rally on Chinese Growth and Mining Merger Speculation

European Stocks Rally on Chinese Growth and Mining Merger Speculation  ECB Keeps July Rate Options Open Amid Iran War Energy Price Risks

ECB Keeps July Rate Options Open Amid Iran War Energy Price Risks  Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed

Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed

The Swiss National Bank (SNB) has maintained status quo in its monetary policy today to leave everything unchanged (kept libor rate at -0.75%). Consequently, the development of CHF over the past weeks did not seem to have provided any reason to tighten the monetary policy reins after all. With lingering uncertainty over the Italian budget conflict and Brexit, CHF seems to be much more in demand again recently. During such a circumstance that the SNB does not want to give the FX market any other arguments for trading the franc at stronger levels, which would put pressure on the inflation outlook and domestic exports.

OTC Updates and Options Strategy:

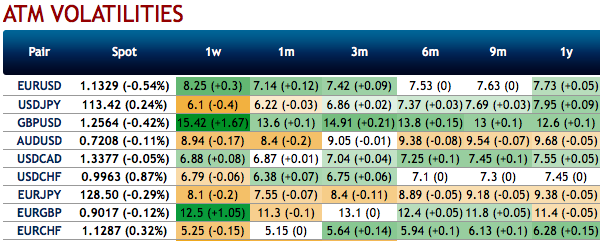

Let’s just quickly glance through above implied volatility (IV) nutshell before deep diving into the strategic frameworks of USDCHF. CHF crosses are showing the least IVs among G10 FX bloc (1m IVs are at 6.38 and 5.15 for USDCHF and EURCHF respectively).

IV factor is highly imperative in FX option dynamics because the option pricing significantly depends on future volatility, and it is quite impossible for any veteran to ascertain accurate future volatility.

Nevertheless, it is quite possible to calculate the marketplace’s expected future volatility using the option’s price itself which is known as implied volatility (IV). Well, this is quite intuitive owing to the higher likelihood of the underlying spot FX market ‘swinging’ in your favour.

If IV increases and you are holding an option, this is good. On the contrary, if you have short on option, it is not desirable. The option writer likes IV to drop so the premium falls, thereby, the underlying price remains stagnant and he can pocket the initial premium received.

The execution of option trading strategy:Contemplating above rationale, the recommendation would be on buying OTM -0.49 delta put while simultaneously shorting ATM put with similar expiries and buy OTM 0.5 delta call while simultaneously shorting an ATM call with similar expiries. This strategy is structured for a larger probability of earning a smaller but certain profit as USDCHF is perceived to have a low volatility.

The highest return for this strategy is achievable when the pair at expiration is equal to the strike price at which the call and put options are sold. At this price, all the options expire worthless and the options trader gets to keep the entire net credit received when entering the trade as profit.

Risk/Returns Profile: The maximum return occurs at ATM strike. A smaller return is made between ATM strikes and the break-even points. The maximum loss is limited by OTM strike prices.

Effect of Volatility: The value of the options will decrease as volatility decreases, which is usually conducive for the strategy. An increase in volatility will be generally bad for the strategy as stated above.

Effect of Time decay: The value of the option decays as each day passes (good).

Margin requirement: Depends on how it is constructed.

Currency Strength Index: FxWirePro's hourly USD spot index is inching towards -98 levels (which is bearish), while hourly CHF spot index was at -56 (bearish), while articulating (at 08:42 GMT). For more details on the index, please refer below weblink: