Global Markets React to Strong U.S. Jobs Data and Rising Yields

Global Markets React to Strong U.S. Jobs Data and Rising Yields  Wall Street Analysts Weigh in on Latest NFP Data

Wall Street Analysts Weigh in on Latest NFP Data  US Gas Market Poised for Supercycle: Bernstein Analysts

US Gas Market Poised for Supercycle: Bernstein Analysts  Bank of America Posts Strong Q4 2024 Results, Shares Rise

Bank of America Posts Strong Q4 2024 Results, Shares Rise  Geopolitical Shocks That Could Reshape Financial Markets in 2025

Geopolitical Shocks That Could Reshape Financial Markets in 2025  Moldova Criticizes Russia Amid Transdniestria Energy Crisis

Moldova Criticizes Russia Amid Transdniestria Energy Crisis  China’s Growth Faces Structural Challenges Amid Doubts Over Data

China’s Growth Faces Structural Challenges Amid Doubts Over Data  U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures

U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures  U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?

U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?  Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close

Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close  Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms

Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms  European Stocks Rally on Chinese Growth and Mining Merger Speculation

European Stocks Rally on Chinese Growth and Mining Merger Speculation  Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes

Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes  UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty

UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty  U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge

U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge  S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays

S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays

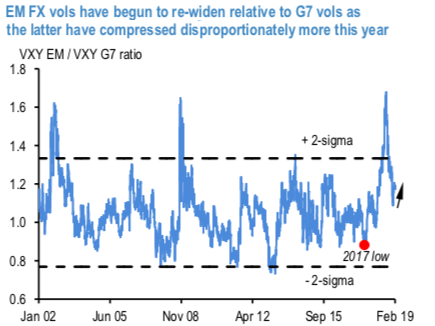

An odd by-product of the nosedive in G7 vol has emerged: EM vs. G7 vol spreads are re-widening, not because risk premia in EM are rising as was the case last year – quite the opposite in fact – but because G7 options have cheapened disproportionately more (refer 1st chart).

Rewards from outright vol selling are absolute, not relative quantities, yet this comparative EM – G7 vol set-up is motivating many to consider short EM FX vol plays as a complement to long carry portfolios. One cannot argue with a theme that is so manifestly working – 2nd chart displays that conventional high-beta EM names like TRY, MXN and KRW led the short vol league tables so far, with sizeable 1.5 – 3.0 % pt. P/Ls, in contrast to mild losses from selling AUD and NZD vol where central bank and data-driven spot gyrations were more acute.

We ourselves are running short TRY and MXN vol in our model portfolio in more cautious formats than outright straddles (TRY – ratio USD put/TRY call spreads; MXN – calendar risk-reversals).

TRY in particular offers above-average vol risk premium to monetize (1M ATM 13.0 vs. trailing 1m realized vol 8.0); we think implied vols are being kept artificially elevated by macro demand for directional carry- earning purchased option structures (USD puts/put spreads/digitals), but the historical track records of cash FX carry versus vol carry in the lira are so starkly divergent (refer 3rd chart) that we think levered money will be drawn to the latter sooner or later, which in turn should pressure vol lower. Courtesy: JPM

Currency Strength Index: FxWirePro's hourly USD spot index is inching towards 3 levels (which is absolutely neutral) while articulating (at 13:14 GMT).

For more details on the index, please refer below weblink: http://www.fxwirepro.com/currencyindex