Geopolitical Shocks That Could Reshape Financial Markets in 2025

Geopolitical Shocks That Could Reshape Financial Markets in 2025  Moldova Criticizes Russia Amid Transdniestria Energy Crisis

Moldova Criticizes Russia Amid Transdniestria Energy Crisis  Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close

Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close  US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts

US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts  UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data

UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data  U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures

U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures  Bank of America Posts Strong Q4 2024 Results, Shares Rise

Bank of America Posts Strong Q4 2024 Results, Shares Rise  UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty

UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty  China’s Growth Faces Structural Challenges Amid Doubts Over Data

China’s Growth Faces Structural Challenges Amid Doubts Over Data  BOJ Rate Hike Expectations Grow as Board Member Signals Hawkish Stance

BOJ Rate Hike Expectations Grow as Board Member Signals Hawkish Stance  ECB Rate Outlook: Ceasefire Eases Pressure but Hikes Still Expected in 2026

ECB Rate Outlook: Ceasefire Eases Pressure but Hikes Still Expected in 2026

The popular explanation for the drop in the franc in 2H’17 emphasizes the currency’s role as a negative yielding, safe-haven and its vulnerability to a continued rally in risk assets together with the rehabilitation of the Euro (many in the market view the franc as little more than the anti-euro).

Based on this framework, CHF continues to be vulnerable to a freeing up of the private capital outflows from Switzerland that have been in abeyance for a decade, both through a repatriation of safe-haven investments by non-residents and a reduction in the defensive home-market bias of Swiss investors.

While we are skeptical of the ‘wall of money’ argument for trend depreciation in the franc, we nevertheless recognize that there is a certain pent-up demand from a range of players to sell the currency.

These include a modest repatriation of foreign-held CHF deposits (the CHF 15bn outflow since the summer equates to 2% of GDP, with perhaps another CHF2530bn more to follow – refer above chart), renewed funding in the franc from short-term FX players if not longer-term, nonresident liability managers, and some selling by Swiss portfolio managers. Of these, an accelerated and potentially concentrated offshore diversification by Swiss investors poses the more significant risk to CHF.

We estimate pent-up capital outflows (excluding bonds as these are liable to be FX-hedged) at CHF 30-85bn. This averages out to 8.5% of GDP, so just a little less than the annual current account surplus for one year.

Sell 3m EURCHF 1.03 - 1.085 strangle against short EURCHF spot.

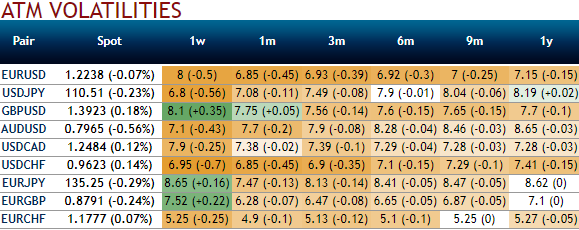

Please have a glance through the implied volatilities of EURCHF ATM contracts from the above nutshell, IVs of this underlying pair of all expiries have still been the least among G10 currency segment despite this week’s ECB’s monetary policy announcement which is significant. These lower volatile conditions are conducive for the option writers.

Let’s be noted that the 25-delta risk of reversal of EURCHF has also not been indicating any dramatic shoot up nor any slumps, but bearish neutral risk reversals indicate that this pair to have been hedged for the downside risks as it indicates puts have been relatively costlier.

The persistent euro strength should nudge EURCHF higher but significantly. As a result, chances of calls being priced exorbitantly. 2w IV skews have been well balanced on both OTM call and put strikes.

As a result, we recommend below option strategies using right options, thereby, one can benefit from certain returns.

Naked Strangle Shorting:

Short 2m OTM put (2% strike difference referring lower cap) and short OTM call simultaneously of the same expiry (2% strike referring upper cap) (we reiterate, comparatively short term for maturity is desired).

Overview: Slightly bearish in short-term but sideways in the medium term.

Timeframe: 3 months

When you write an option, the seller wants IV to remain lower level or to shrink so the premium also fades away.

Hence, writing such calls seems smart choice in tepid IVs on speculative or trading grounds.

Considering above OTC market reasoning, amid prevailing uptrend we think downside risks can also not to be disregarded in the long term, as result we reckon deploying shorts in such exorbitant call options.

FxWirePro launches Absolute Return Managed Program. For more details, visit: