FxWirePro: GBP/USD rises as weak U.S. jobs data pressures dollar

FxWirePro: GBP/USD rises as weak U.S. jobs data pressures dollar  FxWirePro: AUD/USD eases as investors switch focus to RBA

FxWirePro: AUD/USD eases as investors switch focus to RBA  DAX & CAC40 Score Perfect 100: Extremely Bullish With Major Levels to Watch as FTSE100 Hits 80

DAX & CAC40 Score Perfect 100: Extremely Bullish With Major Levels to Watch as FTSE100 Hits 80  FxWirePro: AUD/USD eases as investors await U.S. employment figures

FxWirePro: AUD/USD eases as investors await U.S. employment figures  Major Pair Currency Score: NZD/USD and AUD/USD Lead Forex Rally with Perfect 100 Scores

Major Pair Currency Score: NZD/USD and AUD/USD Lead Forex Rally with Perfect 100 Scores  FxWirePro: GBP/AUD under pressure after disappointing U.S. employment data

FxWirePro: GBP/AUD under pressure after disappointing U.S. employment data  FxWirePro- Major Pair levels and bias summary

FxWirePro- Major Pair levels and bias summary  FxWirePro: EUR/AUD slips after surprise U.S. employment data

FxWirePro: EUR/AUD slips after surprise U.S. employment data  NZDJPY Bears Lie in Wait: Sell Rallies at 93 for 90 Target with 94 Stop

NZDJPY Bears Lie in Wait: Sell Rallies at 93 for 90 Target with 94 Stop  FxWirePro: EUR/ AUD neutral in the near term, scope further downside

FxWirePro: EUR/ AUD neutral in the near term, scope further downside  FxWirePro : EUR/NZD holding below 38.2% fibo ahead of US data

FxWirePro : EUR/NZD holding below 38.2% fibo ahead of US data  FxWirePro: GBP/AUD eases slightly, focus on near-term support

FxWirePro: GBP/AUD eases slightly, focus on near-term support  FxWirePro- Major Crypto levels and bias summary

FxWirePro- Major Crypto levels and bias summary  FxWirePro- Major Pair levels and bias summary

FxWirePro- Major Pair levels and bias summary  FxWirePro- Major Crypto levels and bias summary

FxWirePro- Major Crypto levels and bias summary  FxWirePro: USD/JPY holds tight range ahead of key U.S. payrolls data

FxWirePro: USD/JPY holds tight range ahead of key U.S. payrolls data  Bitcoin Reclaims $65,000 as Easing Geopolitical Tensions Fuel Risk-On Rally

Bitcoin Reclaims $65,000 as Easing Geopolitical Tensions Fuel Risk-On Rally

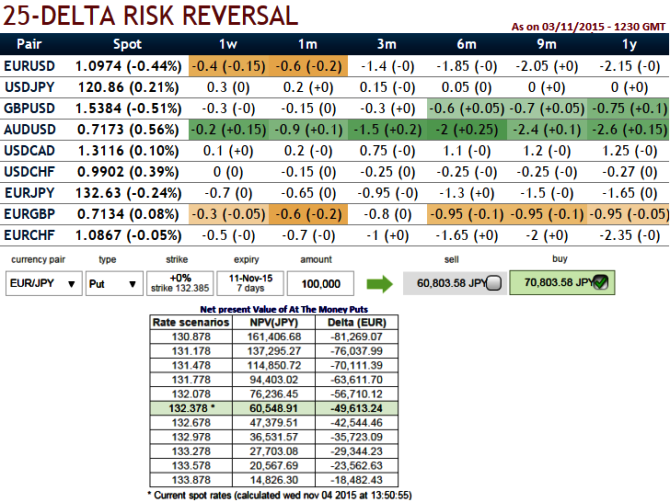

Please observe in the above nutshell how delta risk reversal numbers are inching higher into negative values gradually in a long run (flashing at negative 1.65 for 1 year expiries).

1W at the money 49.6% delta puts are trading 17% higher than NPV.

The current spot FX is trading at 132.388, our earlier targets achieved at 133.372, for now we expect dips extending up to 131.025 levels in near terms. It is understood that bearish momentum is bolstering as we saw that from delta risk reversal table. Hence, aggressive bears can initiate strategy using ATM puts.

The broader the strike difference between short and long puts, the fewer puts you need to sell to cover the price of the long puts.

But at the same time, the coverage of long-to-short is going to be more difficult in the event of assignment.

So, the recommendation for aggressive bears is to add an extra long on put with 1m expiry to the existing debit put spreads and fresh backspreads can built in capitalizing on overpriced ATM puts on short side with 1w expiries.

Since the option you sell will always be lower on the skew curve it means you are getting a better deal on what you are selling compared to what you are buying.

It makes this strategy a good one if the skew is running a little hot but EURJPY hasn't rolled over that much.

However, on a long term hedging perspective, debit put spreads are advocated as the selling indications are piling up on weekly graph. So buying In-The-Money Puts and to reduce the cost of hedging by financing this long position, selling an Out-Of-The-Money put option is recommended.

- News

- Economy

- Central Banks

- Investing

- Research

- Roundups

- Digital Currency

- Insights

- Technical Analysis

- Technology

- Business

- Law

- Health

- Nature

- Fintech

- Science

- Topic

- Opinions

- ©Econometrics LLC . All Rights Reserved.

FxWirePro: Stay Short on EUR/JPY via BPS for risk averse backspreads aggressive bears

Wednesday, November 4, 2015 8:36 AM UTC

Editor's Picks

- Market Data

Most Popular