China Keeps Loan Prime Rates Unchanged for 13th Straight Month as Policymakers Prioritize Credit Demand Recovery

China Keeps Loan Prime Rates Unchanged for 13th Straight Month as Policymakers Prioritize Credit Demand Recovery  Europe Heatwave Creates Growth Opportunity for Carrier, Trane, and Johnson Controls, Citi Says

Europe Heatwave Creates Growth Opportunity for Carrier, Trane, and Johnson Controls, Citi Says  Oil Prices Slip as U.S.-Iran Peace Talks and Strait of Hormuz Risks Keep Markets on Edge

Oil Prices Slip as U.S.-Iran Peace Talks and Strait of Hormuz Risks Keep Markets on Edge  Despite its best efforts, Iran won’t be able to toll the Strait of Hormuz. Here’s why

Despite its best efforts, Iran won’t be able to toll the Strait of Hormuz. Here’s why  U.S. Stocks End Q2 Higher as Strong Jobs Data and AI Rally Lift Wall Street

U.S. Stocks End Q2 Higher as Strong Jobs Data and AI Rally Lift Wall Street  ECB Keeps July Rate Options Open Amid Iran War Energy Price Risks

ECB Keeps July Rate Options Open Amid Iran War Energy Price Risks  Global Financial Firms Shift Asia Expansion Focus to South Korea as China, India Face Caution

Global Financial Firms Shift Asia Expansion Focus to South Korea as China, India Face Caution  Greece’s Bad Loan Crisis Continues to Limit Credit Access Despite Economic Recovery

Greece’s Bad Loan Crisis Continues to Limit Credit Access Despite Economic Recovery  BOJ Rate Hike Expectations Rise as Weak Yen and Strong U.S. Jobs Data Increase Pressure

BOJ Rate Hike Expectations Rise as Weak Yen and Strong U.S. Jobs Data Increase Pressure  Asian Currencies Stay Range-Bound as Investors Eye China Data, RBNZ Outlook and U.S.-Iran Ceasefire

Asian Currencies Stay Range-Bound as Investors Eye China Data, RBNZ Outlook and U.S.-Iran Ceasefire  Elon Musk is remaking the world, like Henry Ford before him – but more dangerously

Elon Musk is remaking the world, like Henry Ford before him – but more dangerously  Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes

Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes  Trump Questions Housing Bill as He Prioritizes SAVE America Act

Trump Questions Housing Bill as He Prioritizes SAVE America Act  In a rebuke to Trump, the Supreme Court rules that birthright citizenship is the law of the land

In a rebuke to Trump, the Supreme Court rules that birthright citizenship is the law of the land  BOJ Raises Interest Rates to 1% as Inflation Pressures Persist

BOJ Raises Interest Rates to 1% as Inflation Pressures Persist

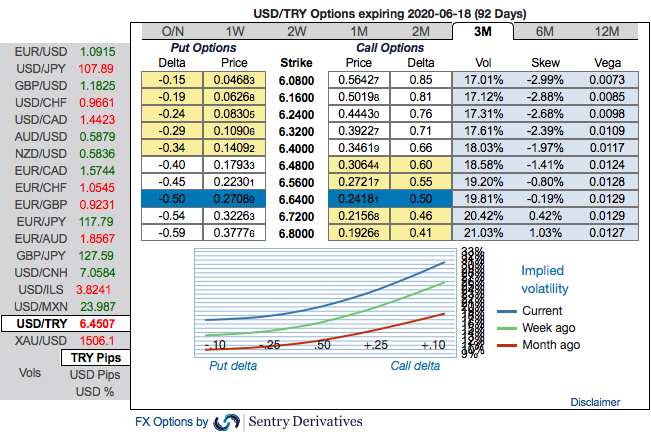

Turkey's central bank pulled forward a scheduled MPC meeting by two days and implemented a 100bps emergency rate cut yesterday. The CB reduced the 1-week repo rate from 10.75% to 9.75% and lowered RRR on all FX deposits by 500bps (for banks which are meeting loan growth criteria); CBT will also provide liquidity to banks using special intraday and overnight facilities as well as 91-day repos if necessary. CBT has increased the liquidity limit on primary dealers, which means that it will effectively fund them at 8.25% instead of the 9.75% policy rate. Having witnessed similar packages launched in recent days by major world central banks as well as several emerging market central banks, NBP for example, CBT's measures fall within a 'reasonable spectrum'. Such measures are being used to mitigate the worst side-effects of the coronavirus outbreak; they are, of course, not intended to solve the underlying healthcare problem, just dampen the collateral damage to the economy. Turkish GDP growth and inflation will both fall in coming months; at this time, the usual consideration of above-target inflation warranting higher interest rates is temporarily on hold. Rate cuts are more likely to have a positive impact on the currency because, without monetary easing, the economy would contract even more. This is why the lira outperformed peers notably following the announcement.

Since the latest data tell us that longstanding Turkish risks still persist, and meanwhile the real interest rate is going to negative, we should look for a sharp rise in USDTRY in coming months.

Hedging Strategy:

On hedging grounds, capitalizing on prevailing price dips and above driving forces, we already advocated 2m USDTRY debit call spreads with a view to arresting momentary downside risks and upside risks in the major trend. At spot reference: 6.4511 level, initiated 2m 6.05/6.80 call spreads at net debit. One can achieve hedging objective as the deep in the money call option with a very strong delta will move in tandem with the underlying spikes.

It seems that hedgers of TRY are positioned for the upside risks on the above fundamental factors. The skewness in 3m IVs are still indicating upside risks, higher bids for OTM calls are hedging bias towards upside risks (refer above nutshell).

IVs of this underlying pair is also on the higher side, trending highest among the G20 FX space. Call options with a higher IVs cost more, because, increasing IV is conducive for the option holder, just for an intuition that the higher likelihood of the market ‘swinging’ in holder’s favour. Courtesy: Sentry & Commerzbank