Bank of Japan Signals Potential Rate Hike as Inflation Risks Rise Amid Energy Shock

Bank of Japan Signals Potential Rate Hike as Inflation Risks Rise Amid Energy Shock  BOJ Governor Kazuo Ueda Hints at Rate Hike as Inflation Pressures Build

BOJ Governor Kazuo Ueda Hints at Rate Hike as Inflation Pressures Build  Bank of Korea Signals Potential Interest Rate Hikes as Inflation Remains Elevated

Bank of Korea Signals Potential Interest Rate Hikes as Inflation Remains Elevated  Fed’s Goolsbee Warns Inflation Remains Elevated, Signals Caution on Rate Cuts

Fed’s Goolsbee Warns Inflation Remains Elevated, Signals Caution on Rate Cuts  ECB Signals Possible Interest Rate Move if Inflation Outlook Fails to Improve

ECB Signals Possible Interest Rate Move if Inflation Outlook Fails to Improve  Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes

Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes

With increased focus on repricing and reassessment of DM interest rates and monetary policy, G10 FX forecasts have had more revisions than EM FX forecasts in the past month. The better data has prompted our economists to adopt a more hawkish forecast on several G10 central banks—we no longer expect the RBA to cut rates by 50bp, the Riksbank is now expected to hike rates in April 2018 versus the prior expectation of July and the BoE is now expected to deliver a 25bp rate hike in November this year and two more in 2018.

Asymmetric uptick in G10 vols is more difficult to envision, since the mix of Fed repricing and tax reform optimism may draw a soft floor under the greenback for the time being even if this week’s upturn does not repeat, and coupled with the somewhat panicky unwinding of Euro (and other European FX) longs might leave macro investors less willing to spend option premium to play for EUR resurgence.

In this situation, if one had to pick one Eurobloc currency to buy vol in, our preferred pick would be GBP, especially on the crosses. We continue to believe that the abrupt shift in BoE policy and the attendant possibility of a policy mistake make sterling a fundamentally more uncertain currency than many others.

The range of spot outcomes on cable has now opened up from a previously narrow 1.28-1.30 band to a much wider 1.28 - 1.36 (or higher) which ought to command a higher premium in implied vols than before.

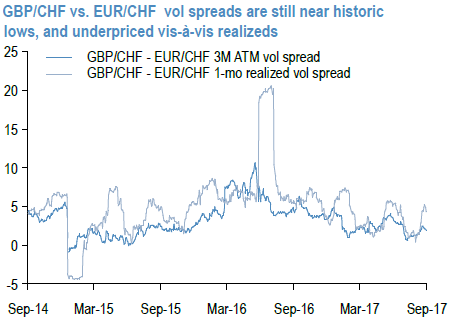

Yet GBP implied vols have retraced 3/4ths of the ramp up from earlier this month, and the recent realized vols are clocking 1 vol above short-dated implieds, hence this appears to be a case of underpriced fundamental uncertainty with supportive technicals for gamma ownership. GBPCHF (GBP vs. CHF implied correlation 40%, realized corrs 35%) in particular strikes as a useful long within the GBP-cross complex, we prefer financing it via shorts in EURCHF.

The GBPCHF – EURCHF vol spread has picked up from 15y lows but is still stuck near the bottom-end of a long-term range, the vol spread has a desirable tendency for one-sided eruptions in favor of a wider GBPCHF premium during market crashes, and enjoys a healthy positive carry at inception (2M ATM vol spread 1.9 mid, realized vol spread 4.0 on 1w and 4w look backs using hourly spot data; refer above chart). Courtesy: JPM