Gold Slips Below $4050 as Bond Yields Surge to 4.7% on Fed Inflation Concerns – Sell Rallies at $4060 Targeting $3940

Gold Slips Below $4050 as Bond Yields Surge to 4.7% on Fed Inflation Concerns – Sell Rallies at $4060 Targeting $3940  3 clinical-grade skincare creams you really shouldn’t buy online

3 clinical-grade skincare creams you really shouldn’t buy online  Is Netanyahu’s star waning in Washington? His latest meeting with Trump suggests it may be

Is Netanyahu’s star waning in Washington? His latest meeting with Trump suggests it may be  World game at war: why some European nations have threatened a World Cup boycott

World game at war: why some European nations have threatened a World Cup boycott  Meta-backed research finds exposure to ‘untrustworthy’ social media is rare. The fine print is less reassuring

Meta-backed research finds exposure to ‘untrustworthy’ social media is rare. The fine print is less reassuring

– place PRBS to reduce hedging cost - EconoTimes)

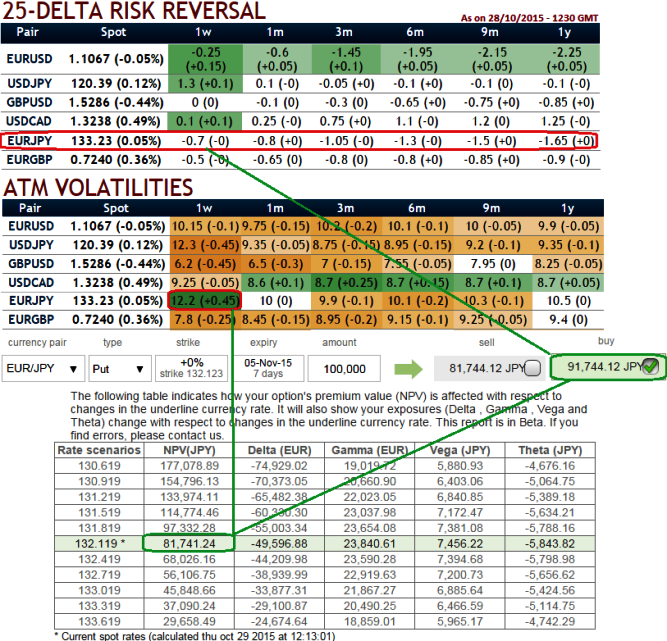

Please observe how delta risk reversal numbers are getting higher negative values gradually in a long run (flashing at negative 1.65 for 1 year expiries).

Volatility smiles most frequently show that traders are willing to pay higher implied volatility prices as the strike price grows aggressively out of the money. (IV grows at 12.2% which is quite higher).

1W At The Money 50% delta puts are trading 13% higher than NPV.

The current spot FX is trading at 136.555, we expect dips extending up to 133.372 levels in near terms. It is understood that bearish momentum is bolstering as we saw that from delta risk reversal table and technical indications. Hence, aggressive bears can initiate strategy using ATM puts.

The broader the strike difference between short and long puts, the fewer puts you need to sell to cover the price of the long puts.

But at the same time, the coverage of long-to-short is going to be more difficult in the event of assignment.

So, the recommendation for now is to add an extra long on put with 1m expiry to the existing debit put spreads and fresh backspreads can built in capitalizing on overpriced ATM puts on short side with 1w expiries.

Since the option you sell will always be lower on the skew curve it means you are getting a better deal on what you are selling compared to what you are buying.

It makes this strategy a good one if the skew is running a little hot but EURJPY hasn't rolled over that much.

- News

- Economy

- Central Banks

- Investing

- Research

- Roundups

- Digital Currency

- Insights

- Technical Analysis

- Technology

- Business

- Law

- Health

- Nature

- Fintech

- Science

- Topic

- Opinions

- ©Econometrics LLC . All Rights Reserved.

FxWirePro: Risk reversals suggest EUR/JPY ATM puts costlier (13% higher NPV) – place PRBS to reduce hedging cost

Thursday, October 29, 2015 7:20 AM UTC

Editor's Picks

- Market Data

Most Popular