Trump has made more than $1 billion from crypto in a year. How?

Trump has made more than $1 billion from crypto in a year. How?  Bank of America Posts Strong Q4 2024 Results, Shares Rise

Bank of America Posts Strong Q4 2024 Results, Shares Rise  Alcohol is one of the most dangerous drugs, yet its presence is ubiquitous in social settings and celebrations

Alcohol is one of the most dangerous drugs, yet its presence is ubiquitous in social settings and celebrations  Buy the Dip: Gold Holds Strong at $3980, Targets $4150

Buy the Dip: Gold Holds Strong at $3980, Targets $4150  Elon Musk is remaking the world, like Henry Ford before him – but more dangerously

Elon Musk is remaking the world, like Henry Ford before him – but more dangerously  S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays

S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays  Vietnam’s population hit the 100 million milestone. Where’s it headed?

Vietnam’s population hit the 100 million milestone. Where’s it headed?  China Sets 1.25% Overnight Reverse Repo Rate Below Market Expectations

China Sets 1.25% Overnight Reverse Repo Rate Below Market Expectations  European Stocks Rally on Chinese Growth and Mining Merger Speculation

European Stocks Rally on Chinese Growth and Mining Merger Speculation  Energy Sector Outlook 2025: AI's Role and Market Dynamics

Energy Sector Outlook 2025: AI's Role and Market Dynamics

Banxico hiked 25bp; we see limited MXN gains but prefer calendar skews at the current juncture.

Banxico has hiked its policy rate 25bp to 6.5% and signaled a shift in gears towards a slower pace of tightening ahead.

Following the policy statement, JPMorgan updates its policy call and now looks for Banxico to hike 25bp in May and keep the policy rate stable at 6.75% thereafter.

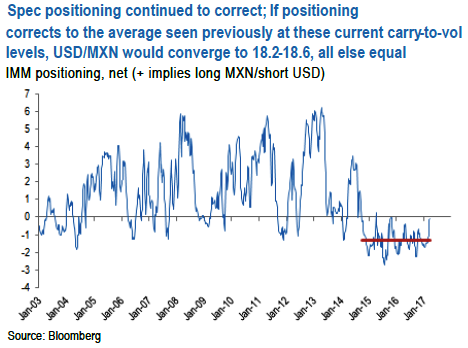

As discussed in a note published last week, attractive carry-to-volatility ratios should help the MXN in the medium term, and speculative positioning seems to have begun reacting to that– the last time carry-to-vol was at current levels, speculative positions were substantially long MXN.

If positioning corrects to the average seen previously at these current carry-to-vol levels, USDMXN would converge to 18.2-18.6, all else equal.

In all, higher Mexican rates and lower volatility make the MXN more attractive as a short-term trade, although we see limited capital gains at these levels.

Next week, the Trump-Xi meeting could cast light on US trade strategy going forward and could reverberate on USDMXN.

In the last few weeks, we have seen a material easing of the anxiety that had built around the NAFTA renegotiations.

Yet, there is no clarity yet on the US administration’s intentions for the NAFTA renegotiation, and we are still wary of the bargaining power that an existing Mexican administration will have, given Mexican Presidential elections are scheduled for June 2018.

As we see risks resurfacing in H2’17 and note that risk reversals look cheap, even when filtering out the impact of the recent ATM vol drop. Thus, we recommend buying gamma neutral calendar skews (sell 3M 25 delta put, buy 6M 25 delta call, in gamma neutral notionals).