Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed

Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed  U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge

U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge  Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms

Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms  Wall Street Analysts Weigh in on Latest NFP Data

Wall Street Analysts Weigh in on Latest NFP Data  JPMorgan Lifts Gold Price Forecast to $6,300 by End-2026 on Strong Central Bank and Investor Demand

JPMorgan Lifts Gold Price Forecast to $6,300 by End-2026 on Strong Central Bank and Investor Demand  Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes

Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes  Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure

Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure  Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand

Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand  China’s Growth Faces Structural Challenges Amid Doubts Over Data

China’s Growth Faces Structural Challenges Amid Doubts Over Data  US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts

US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts  Trump’s "Shock and Awe" Agenda: Executive Orders from Day One

Trump’s "Shock and Awe" Agenda: Executive Orders from Day One

The high uncertainty about the political future of Brazil is not putting pressure on BRL at present. The generally positive market sentiment as well as the credible monetary policy support BRL. If these framework conditions were to change BRL might come under pressure in the run-up to the elections. We expect a continuation of the sideways move in USDBRL for now, but in our view, the risk is clearly pointing to the upside.

It is difficult to predict the outcome of the Presidential elections in October at the moment. The former President Luiz Inácio Lula da Silva has a clear lead in the opinion polls. However, the problem is: he was convicted of corruption last year. On Monday the second application for appeal was rejected. He can still take his appeal further, but the likelihood of him standing in the elections in October seems slim. It is difficult to comment on the rest of the candidates. It is possible that Minister of Finance Henrique Meirelles might stand as a candidate, he will take a decision next week. Moreover, there were reports that the acting President Michel Temer is considering a further term in office.

Along with the above-discussed EUR/EM constructs that take advantage of high carry-to-vol, with the Fed in a slower gear than the markets expected here we widen the net by employing no-touch structures as a passive play on limited upside in high beta FX.

No-touches can be seen as defined downside alternatives to selling naked vanilla high-beta & EM puts and are well suited to take advantage of a modestly risk-positive environment that should emerge after the trade dust settles.

The 1st chart ranks 3M high beta structures with barriers set to 1-sigma away from the spot (arbitrary condition but sets pricing of different pairs on similar footing and strikes us as a sensible barrier selection).

No-touches take advantage of elevated fwd points, vols and skew. Effectively vol selling structures, no-touches are inherently low leverage trades, as is the case for other income harvesting strategies (e.g.vol, carry and vanilla selling).

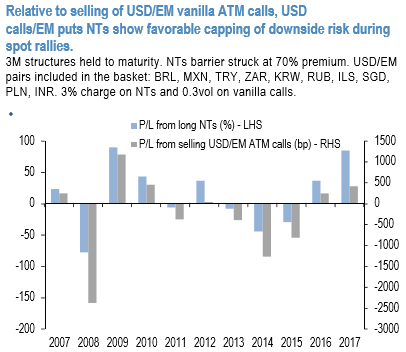

The 2nd chart demonstrates back-testing buying of no-touches relative to selling vanilla USD calls/EM puts for a basket of 10 USD/EM pairs and outlines the capped downside advantage of NTs during the dollar rallies, that makes NT performance d risk-reward characteristics favorable. Courtesy: JPM

Given the analysts’ constructive view on USDBRL and USDRUB and favorable pricing consider:

Buy 3M USDBRL call no-touch with barrier @3.400, the level not breached since Dec 2016, costs 39.5% USD.

Buy 3M USDRUB call no-touch with barrier @59.00, the level not breached since last Dec, costs 45% USD.

FxWirePro launches Absolute Return Managed Program. For more details, visit: