U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures

U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures  China Sets 1.25% Overnight Reverse Repo Rate Below Market Expectations

China Sets 1.25% Overnight Reverse Repo Rate Below Market Expectations  U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge

U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge  BOJ Raises Interest Rates to 1% as Inflation Pressures Persist

BOJ Raises Interest Rates to 1% as Inflation Pressures Persist  Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data

Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data  New Zealand Unemployment and Inflation Debate Intensifies Ahead of 2026 Election

New Zealand Unemployment and Inflation Debate Intensifies Ahead of 2026 Election  BOJ Rate Hike Expectations Rise as Weak Yen and Strong U.S. Jobs Data Increase Pressure

BOJ Rate Hike Expectations Rise as Weak Yen and Strong U.S. Jobs Data Increase Pressure  US Gas Market Poised for Supercycle: Bernstein Analysts

US Gas Market Poised for Supercycle: Bernstein Analysts  China’s Growth Faces Structural Challenges Amid Doubts Over Data

China’s Growth Faces Structural Challenges Amid Doubts Over Data  European Stocks Rally on Chinese Growth and Mining Merger Speculation

European Stocks Rally on Chinese Growth and Mining Merger Speculation  Bank of America Posts Strong Q4 2024 Results, Shares Rise

Bank of America Posts Strong Q4 2024 Results, Shares Rise  Malaysia Central Bank Moves to Support Ringgit Amid Foreign Fund Outflows

Malaysia Central Bank Moves to Support Ringgit Amid Foreign Fund Outflows  Goldman Sachs Sees Fed Holding Interest Rates Steady Until 2027

Goldman Sachs Sees Fed Holding Interest Rates Steady Until 2027

The FX market is not alone in its concerns about weak global growth. An increasing number of central banks are warning of the resulting external risks. Yesterday Riksbank also caved in and assumed a more cautious course; even though it principally sticks to its outlook for a more restrictive monetary policy. It is still planning rate hikes and has even announced to change the reinvestment of the bonds held by the bank in such a manner that its holdings will fall slightly by the end of 2020.

However, what was mainly relevant for the market yesterday was that Riksbank lowered its rate path. EURSEK levels of above 10.60 show clearly that the FX market doubts whether Riksbank will be able to decouple from the developments in the eurozone.

While the outlook for the eurozone remains subdued SEK traders clearly do not expect Riksbank to aggressively hike interest rates to support SEK. There doesn’t seem to be another explanation to why krona is trading at the current weak levels despite Riksbank’s principally more restrictive approach.

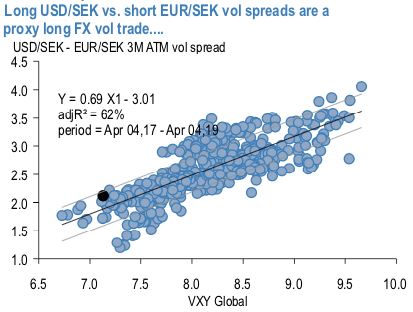

Long USDSEK vs short EURSEK vol spreads is a carry friendly way of owning FX vol from multi-year lows. Owning USD vol over cross-vol has almost always acted as a proxy bullish vol stance owning to the greater risk beta of the USD leg, and USDSEK vs EURSEK is no exception (refer 1stchart). Case in point, the ~2 vol trough-to- peak vol spike in the VXY index during the EM sell-off of Q2-Q3 last year was accompanied by a near-identical move in the USDSEK – EURSEK 3M vol switch. By construction, the spread is more or less immune to idiosyncratic SEK dynamics (if anything, a tad positively geared to krona noise owing once again to USDSEK’s greater beta). The additional appeal is that unlike in most individual currency pairs, implied vs. realized vol technicals are favourable for sustaining the position without stopping out on the decay bill (refer 2ndchart).

Comfortingly, USDSEK also screens as a strong conviction vol buy on our machine learning-based (SVM) gamma trading model (see above nutshell), hence downside to vol ownership there should be limited.

For those averse to any kind of vol ownership in the current climate, it may still be worth considering the short EURSEK leg of the RV above in limited risk format.

The preference is for a 2M 10.30 – 10.65 at-expiry digital EURSEK range (seller of the range collects 44% EUR from selling a 2M 10.30 EURSEK digital put and a 2M 10.65 digital EURSEK call) that eliminates the jump risk of American barriers (DNTs) even if it comes at the cost of markedly reduced leverage (1:2.3 instead of say 5:1).

The macro analysts see EURSEK nearly flat through 2Q (10.40) and only modestly lower around 10.30 in 6-mo time, the lack of excitement in the spot is probably attributable to a slow-moving Riksbank. The range extremes in our preferred structure are skewed to the upside in the spot in deference to the deep malaise in Euro area growth that can potentially extend EURUSD weakness to or below 1.10 in coming months; such Euro weakness has historically been associated with a rise in EURSEK. Courtesy: JPM & Commerzbank

Currency Strength Index: FxWirePro's hourly EUR is at -86 (bearish), hourly USD spot index was at 35 (mildly bullish) while articulating (at 14:11 GMT).

For more details on the index, please refer below weblink: http://www.fxwirepro.com/currencyindex