Bank of Japan's Ueda Flags Low Real Interest Rates as Key Factor in Rate Hike Timing

Bank of Japan's Ueda Flags Low Real Interest Rates as Key Factor in Rate Hike Timing  RBA Rate Hike Outlook: Impact on AUD/USD and ASX 200

RBA Rate Hike Outlook: Impact on AUD/USD and ASX 200  Japan Inflation Expectations Rise as BOJ Rate Hike Timing Faces Uncertainty

Japan Inflation Expectations Rise as BOJ Rate Hike Timing Faces Uncertainty  Bank of Japan Signals Potential Rate Hike as Inflation Risks Rise Amid Energy Shock

Bank of Japan Signals Potential Rate Hike as Inflation Risks Rise Amid Energy Shock  RBA Raises Interest Rates to 4.35% Amid Rising Inflation Risks and Middle East Tensions

RBA Raises Interest Rates to 4.35% Amid Rising Inflation Risks and Middle East Tensions  South Korea Central Bank Signals Inflation Concerns as Oil Prices Surge

South Korea Central Bank Signals Inflation Concerns as Oil Prices Surge

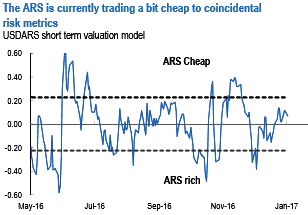

We encourage holding longs in ARS, short USDARS. The peso is currently trading a bit cheap to coincidental risk metrics (refer above chart), helped by soy prices, the positive real rate enforced by the Central Bank to prevent further inflation expectations de-anchoring, and high agricultural export proceeds for the season of the year.

The trade balance posted a US$2.1bn surplus in 2016, a sharp turnaround from the US$3.0bn deficit in 2015.

Imports contracted US$4.1bn last year, explaining 81% of the swing in the trade balance.

2016 primary fiscal deficit (ex.-tax amnesty fiscal inflows) was 6.0% of GDP, well above our 5.0% forecast.

Short USDARS, we remain constructive on ARS and continue to recommend selling 3m and up to 6m USDARS NDF as one of the few carry trades where we expect the positive total return.

The recent macro news supports this outlook, as our nowcaster suggests that Q4’16 GDP expanded by 5% QoQ SAAR, materially better than our prior 3.2% forecast.

Stay short in USDARS via 6-month NDF (sell at 15.86).