Malaysia Central Bank Moves to Support Ringgit Amid Foreign Fund Outflows

Malaysia Central Bank Moves to Support Ringgit Amid Foreign Fund Outflows  Trump has made more than $1 billion from crypto in a year. How?

Trump has made more than $1 billion from crypto in a year. How?  China Sets 1.25% Overnight Reverse Repo Rate Below Market Expectations

China Sets 1.25% Overnight Reverse Repo Rate Below Market Expectations  Wall Street Analysts Weigh in on Latest NFP Data

Wall Street Analysts Weigh in on Latest NFP Data  BoE Policymaker Alan Taylor Signals No Need for Interest Rate Hike Amid Iran War Inflation Risks

BoE Policymaker Alan Taylor Signals No Need for Interest Rate Hike Amid Iran War Inflation Risks  Goldman Sachs Sees Fed Holding Interest Rates Steady Until 2027

Goldman Sachs Sees Fed Holding Interest Rates Steady Until 2027  Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data

Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data  BOJ Raises Interest Rates to 1% as Inflation Pressures Persist

BOJ Raises Interest Rates to 1% as Inflation Pressures Persist  Global Markets React to Strong U.S. Jobs Data and Rising Yields

Global Markets React to Strong U.S. Jobs Data and Rising Yields  RBA Expected to Hold Interest Rates at 4.35% as Markets Watch AUD/USD and ASX 200

RBA Expected to Hold Interest Rates at 4.35% as Markets Watch AUD/USD and ASX 200  In a rebuke to Trump, the Supreme Court rules that birthright citizenship is the law of the land

In a rebuke to Trump, the Supreme Court rules that birthright citizenship is the law of the land  Energy Sector Outlook 2025: AI's Role and Market Dynamics

Energy Sector Outlook 2025: AI's Role and Market Dynamics  2025 Market Outlook: Key January Events to Watch

2025 Market Outlook: Key January Events to Watch  UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty

UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty  New Zealand Unemployment and Inflation Debate Intensifies Ahead of 2026 Election

New Zealand Unemployment and Inflation Debate Intensifies Ahead of 2026 Election

The semi-annual Congressional testimony of Fed chair Janet Yellen was the most important event of this week – so far. Not surprisingly, it did not reveal anything new in comparison to the minutes of the FOMC’s June meeting: Inflation will be the key factor for any decisions about rate hikes. The recent re-pricing in rates markets for DM central banks appears stretched for some countries, in particular for CAD and NZD. Canada would be of interest ahead of the BoC next week given the recent hawkish shift by the central bank.

Dollar bears may be frustrated by Fed tightening and a reluctance to tolerate stronger currencies elsewhere. The clearest winner should be the euro, as the ECB can’t normalize policy (even slowly) and expect current valuations to persist, but it won’t like that much.

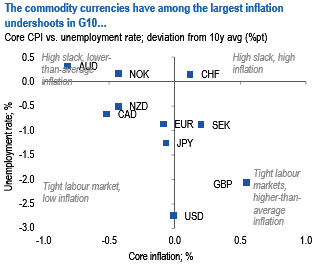

The above chart shows that Canada’s inflation undershoot is larger than that of the US and labour markets nowhere as tight, yet markets price in similar policy rates by the end of 2018.

We thus have a bearish bias on CAD going into the meeting although relatively strong data momentum in Canada and the unexpected nature of BoC’s shift means that overall exposure to this is relatively light (we are implicitly short CAD vs USD through DXY).

Similarly, the Antipodean strategists think that the rates markets price in too much for the RBNZ. We are short NZD in the recommended portfolio but this is maintained vs. BRL. The expectation of a limited bond market sell-off also indicates that EM weakness should be contained as well.

The EM strategists have net reduced risk in EMEA EM but only to currencies which are most vulnerable. We thus maintain long exposure to select EM currencies where idiosyncratic factors are still supportive. This includes long CZK and ILS among the low-yielders. Exposure to high yielders like TRY and BRL are held versus other high beta currencies with lower carry, specifically ZAR and NZD to reduce beta to changes in risk sentiment. These currencies also have similar betas to yields so such pairings provide the cushion against higher yields as well (refer the second chart).

The resulting portfolio is thus positioned on primarily the following themes: in G10, short global rates (via short EURJPY outright and through call RKO), selectively long carry in low-beta format (short NZDBRL, long TRYZAR) and long currencies with strong idiosyncratic drivers (long ILS on strong external balances, long CZK on policy normalization and valuations).