U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures

U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures  Trump’s "Shock and Awe" Agenda: Executive Orders from Day One

Trump’s "Shock and Awe" Agenda: Executive Orders from Day One  Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms

Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms  US Gas Market Poised for Supercycle: Bernstein Analysts

US Gas Market Poised for Supercycle: Bernstein Analysts  UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data

UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data  BTC Flat at $89,300 Despite $1.02B ETF Exodus — Buy the Dip Toward $107K?

BTC Flat at $89,300 Despite $1.02B ETF Exodus — Buy the Dip Toward $107K?  Elon Musk’s Empire: SpaceX, Tesla, and xAI Merger Talks Spark Investor Debate

Elon Musk’s Empire: SpaceX, Tesla, and xAI Merger Talks Spark Investor Debate  UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty

UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty  Global Markets React to Strong U.S. Jobs Data and Rising Yields

Global Markets React to Strong U.S. Jobs Data and Rising Yields

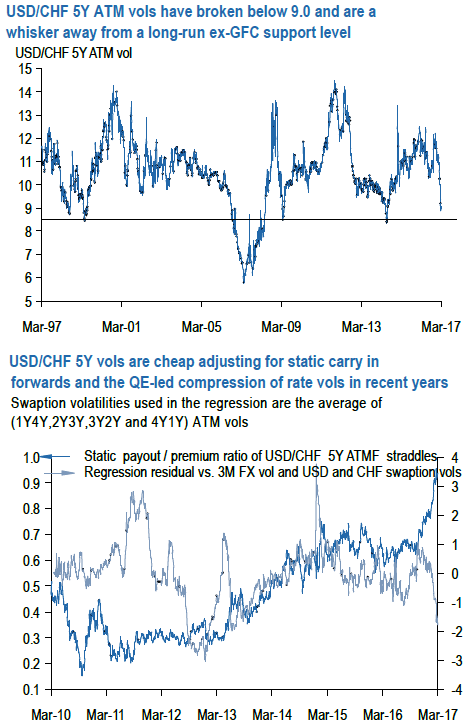

The back-end (5Y and out) USDCHF vol is beginning to approach deep value levels. While not quite through Q2’14 lows that we flagged in reference to USDJPY last week, 5Y ATMs have cratered in excess of 3 % pts and broken below 9.0 for the first time since that Great Moderation 2.0 period, and are a whisker away from a long-run ex-GFC floor (refer above chart). A few other valuation –related observations:

Adjusted for short-dated (3M) FX vol and blended (1Y4Y, 2Y3Y, 3Y2Y, 4Y1Y) USD and CHF swaptions vols, 5Y ATMs look ~1.5 pts. too low (refer above chart).

The result is robust to the inclusion/otherwise of illiquid CHF swaptions, and suggests that the decline in long-end FX vol has undershot the QE-driven compression of interest rate volatility.

Carry/vol ratios of 5Y ATMF straddles are the highest in the post-GFC era, helped by the widening US-Swiss rate gap over the past few years (refer above chart).

In fact, forward points are large enough now to almost cover the entire straddle premium, and USDCHF outranks every other G10 currency on this metric including traditional carry heavyweights such as AUD and NZD.

Carry in forwards aside, slide along the vol surface is the other significant component of overall option bleed; in this respect, the flattening of the 5Y- 1Y vol curve since last year (current +0.8 pts from 2 vols + in Q3’16) is helpful, though there is still some way to travel before hitting the pancake flat plateau of the pre-2007 years.