US Gas Market Poised for Supercycle: Bernstein Analysts

US Gas Market Poised for Supercycle: Bernstein Analysts  3 clinical-grade skincare creams you really shouldn’t buy online

3 clinical-grade skincare creams you really shouldn’t buy online  Meta-backed research finds exposure to ‘untrustworthy’ social media is rare. The fine print is less reassuring

Meta-backed research finds exposure to ‘untrustworthy’ social media is rare. The fine print is less reassuring  China’s Growth Faces Structural Challenges Amid Doubts Over Data

China’s Growth Faces Structural Challenges Amid Doubts Over Data  U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge

U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge  Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed

Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed  S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays

S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays  US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts

US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts  2025 Market Outlook: Key January Events to Watch

2025 Market Outlook: Key January Events to Watch  Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes

Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes  Moldova Criticizes Russia Amid Transdniestria Energy Crisis

Moldova Criticizes Russia Amid Transdniestria Energy Crisis  SpaceX Earnings Preview: Bernstein Says 4 Key Factors Will Drive Long-Term Valuation

SpaceX Earnings Preview: Bernstein Says 4 Key Factors Will Drive Long-Term Valuation  Ukraine’s drone strikes are having an impact on Russia — but Russian leaders remain committed to war

Ukraine’s drone strikes are having an impact on Russia — but Russian leaders remain committed to war  Geopolitical Shocks That Could Reshape Financial Markets in 2025

Geopolitical Shocks That Could Reshape Financial Markets in 2025

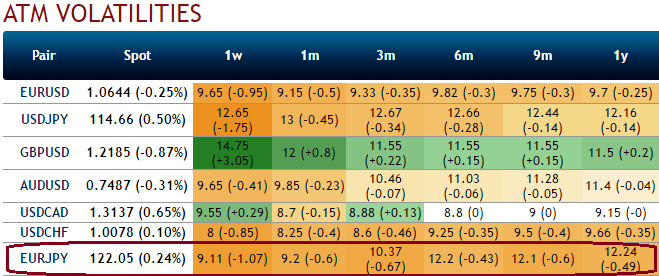

The EUR/JPY volatility surface is offering very attractive opportunities because the skew on the 6m and 1y is currently excessive (refer 4th graph). Where IV skews seem to be mispricing, which is why implied vols of this pair across the various tenors are reducing considerably.

If we’ve to contemplate that the options market is pricing EURJPY risk reversals (RR) as the sum of EUR/USD and USD/JPY RR, the triangle is perfectly priced (refer 2nd graph). The implied volatility of 6m and 1y 25-delta strikes is trading about 3 volatility points higher than ATM volatility, which supposes that the implied volatility should be strongly negatively correlated with the FX rate.

Since 2013, the EURJPY RR has strongly mean reverted towards the vol/spot correlation. However, this correlation has been about zero for a few weeks (refer 3rd graph), such that EURJPY 6m skew is now disconnected from its fair value.

Splitting the EURJPY RR into EURUSD and USDJPY components, like the market, exhibits the source of this mispricing. The EURUSD 6m RR is trading at -1.8 and the USD/JPY at -1.1. The former is consistent with the EURUSD price action, which actually saw downside volatility.

However, USDJPY has indeed been positively correlated with its volatility, hence the EURJPY mispricing comes from the yen side. Investors could directly consider selling the USDJPY excessive skew, but we recommend selling the EURJPY skew instead. It offers a larger risk premium (due to the fairly priced EURUSD smile component), which is opportunistic given our bullish bias on the spot.