BOJ Raises Interest Rates to 1% as Inflation Pressures Persist

BOJ Raises Interest Rates to 1% as Inflation Pressures Persist  Despite its best efforts, Iran won’t be able to toll the Strait of Hormuz. Here’s why

Despite its best efforts, Iran won’t be able to toll the Strait of Hormuz. Here’s why  Trump has made more than $1 billion from crypto in a year. How?

Trump has made more than $1 billion from crypto in a year. How?  Mary Daly Says AI Uncertainty Clouds Fed Rate Outlook Despite Restrictive Policy

Mary Daly Says AI Uncertainty Clouds Fed Rate Outlook Despite Restrictive Policy  BOJ Hawk Signals Faster Interest Rate Hikes Amid Inflation Risks

BOJ Hawk Signals Faster Interest Rate Hikes Amid Inflation Risks  South Korea Signals Possible Interest Rate Hike as Inflation Remains Elevated

South Korea Signals Possible Interest Rate Hike as Inflation Remains Elevated  Taiwan Central Bank Likely to Keep Interest Rates Unchanged Through 2027

Taiwan Central Bank Likely to Keep Interest Rates Unchanged Through 2027  Alcohol is one of the most dangerous drugs, yet its presence is ubiquitous in social settings and celebrations

Alcohol is one of the most dangerous drugs, yet its presence is ubiquitous in social settings and celebrations  Morgan Stanley Names BAE Systems Top European Defence Stock Despite Lower Price Target

Morgan Stanley Names BAE Systems Top European Defence Stock Despite Lower Price Target

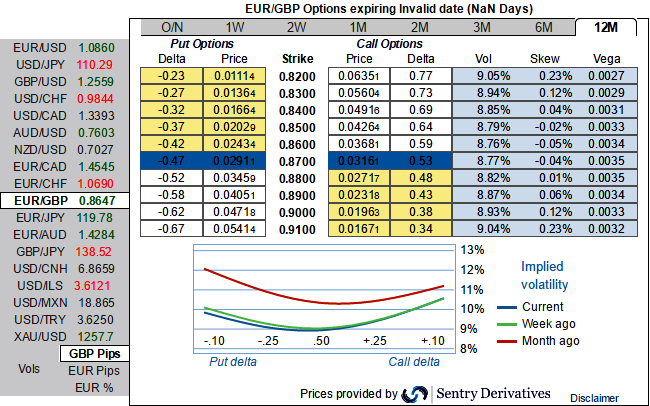

EURGBP moved slightly lower and Gilt yields ticked 4bp higher driven by the more hawkish tone in the statement, where Kristin Forbes voted for a 25bp rate hike this time. Note, however, that Forbes is a known hawk and leaves the BoE this summer.

• The market is now pricing in an accumulated 8bprate hike from the BoE in 2017 and 26bpby the end of 2018. We still think the market’s pricing is too hawkish, suggesting little support for the GBP driven by higher UK interest rates ahead. Hence, relative rates, in our view, favor lower GBPUSD, as the Fed is slightly underpriced, while risks stemming from relative rates are more balanced for EURGBP, as the market has turned too hawkish on the ECB pricing as well, with a 10bp rate hike priced by March 2018.

• EURGBP has fallen back below our 1-3M target of 0.87. As such, we still see risks skewed on the upside for EURGBP, as we expect GBP to underperform vis-à-vis the USD and EUR in coming weeks and following the triggering of Article 50.

• However, the Brexit risk premium priced on GBP has increased over the past two to three weeks and, given that investors are very short GBP, according to IMM, further GBP short covering could pave the way for a short-term correction lower in EURGBP.

Please be noted that the IVs and skews are conducive for call option holders.

As you can probably guess from the positively skewed IVs across all tenors (inclusive of 1Y tenor) signifying the hedgers’ interests for upside risks, as a result OTC market environment lures OTM call option holders’ opportunities. While an option holder wants higher IV or IVs to spike further so that the premium would also grow higher accordingly which could be the conducive case here if we have to evaluate OTC tools.