US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts

US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts  Eurozone Bond Yields Fall as Oil Slump Eases Inflation Fears Ahead of Central Bank Meetings

Eurozone Bond Yields Fall as Oil Slump Eases Inflation Fears Ahead of Central Bank Meetings  Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure

Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure  Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data

Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data  Global Markets React to Strong U.S. Jobs Data and Rising Yields

Global Markets React to Strong U.S. Jobs Data and Rising Yields  2025 Market Outlook: Key January Events to Watch

2025 Market Outlook: Key January Events to Watch  Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes

Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes  Energy Sector Outlook 2025: AI's Role and Market Dynamics

Energy Sector Outlook 2025: AI's Role and Market Dynamics  China Holds Loan Prime Rates Steady for 14th Month as Economic Recovery Remains Uneven

China Holds Loan Prime Rates Steady for 14th Month as Economic Recovery Remains Uneven  BOJ Rate Decision in Focus as Sticky Inflation, Weak Yen Shape USD/JPY and Nikkei Outlook

BOJ Rate Decision in Focus as Sticky Inflation, Weak Yen Shape USD/JPY and Nikkei Outlook  China's Refining Industry Faces Major Shakeup Amid Challenges

China's Refining Industry Faces Major Shakeup Amid Challenges  South Korea Raises Interest Rates to 2.75% as Inflation and Weak Won Drive Tightening

South Korea Raises Interest Rates to 2.75% as Inflation and Weak Won Drive Tightening

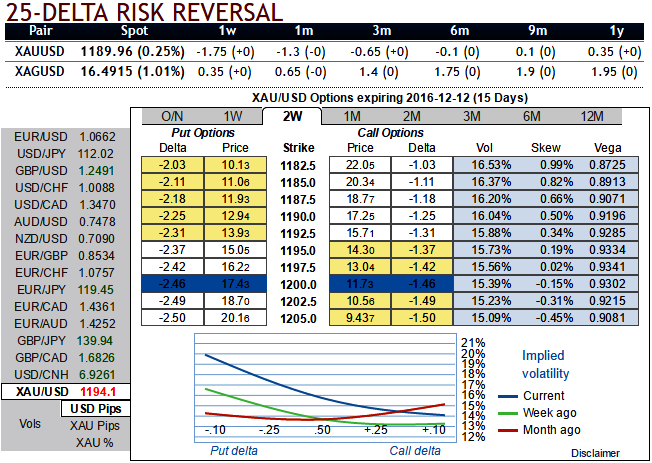

Gold futures contracts for December delivery was trading at $1,191.5 a troy ounce while articulating, after earlier rising as high as $1,197.00 on account of dollar strength.

OTC outlook:

As you can observe the risk reversal flashes for 1 and 3 months tenors, bears in gold prices seem to have more traction ahead of Federal reserve monetary policy announcements, whereas dollar is also likely to risk in 3m tenor, i.e on eve of Christmas where Fed’s chances of hiking can’t be disregarded.

Mounting negative risk reversals coupled with 1m skews would mean that the underlying gold prices likely to slide further and suggests RKO calls on speculative grounds, and 1w-1m skew has been bid with after Trump’s series of speculation and now posing mightier dollar owing to Fed’s booster may lift it to its highest level since June 2015, but in short run underlying precious metal losing the importance of safe-haven sentiment that has been lingering from the recent past.

So, we reckon above fundamentals seem to be addressed by hedging participants via gold’s option market set up. We too accordingly come up with suitable hedging framework considering these developments.

Hedging strategy:

Strategy: 3-Way Diagonal Straddle versus OTM Call

Spread ratio: (Long 1: Long 1: Short 1)

Rationale: Let’s glance on sensitivity tool for 2w IV skews (you could even check for 1m tenors) would signify the interests of OTM put strikes that means the ATM calls higher likelihood of expiring in-the-money.

The execution:

Go long in XAUUSD 1M at the money -0.49 delta put, and go long 1M at the money +0.51 delta call and simultaneously, writing 2W (1%) out of the money call with positive theta. One can initiate strategy as shown in the diagram but please be noted that the tenors shown in the diagram are just for the demonstration purpose, use suitable tenors as per your requirement.

Favor optionality to directional trades. We are inclined to position for a partial retracement of the down move through call spreads, as calling the bottom is difficult and adding directional spot exposure is risky at the moment. For speculators, call spreads are preferred to vanilla structures given elevated skew and favorable cost reduction.