Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data

Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data  Urban studies: Doing research when every city is different

Urban studies: Doing research when every city is different  UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty

UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty  Global Markets React to Strong U.S. Jobs Data and Rising Yields

Global Markets React to Strong U.S. Jobs Data and Rising Yields  2025 Market Outlook: Key January Events to Watch

2025 Market Outlook: Key January Events to Watch  Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure

Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure  Fed May Resume Rate Hikes: BofA Analysts Outline Key Scenarios

Fed May Resume Rate Hikes: BofA Analysts Outline Key Scenarios  Stock Futures Dip as Investors Await Key Payrolls Data

Stock Futures Dip as Investors Await Key Payrolls Data  Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close

Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close  S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays

S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays  Nasdaq Proposes Fast-Track Rule to Accelerate Index Inclusion for Major New Listings

Nasdaq Proposes Fast-Track Rule to Accelerate Index Inclusion for Major New Listings

The global picture on the volatility front hasn’t really changed in recent months. Implied and realized volatility is still hovering in their low or very low percentiles. The currency market has been acting as the adjustment factor between countries positioned at different parts of the economic cycle clock built.

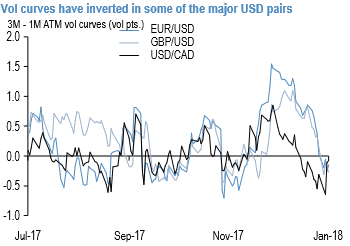

The eye-catching jump in front-end USD vols of late -VXY Global is up 0.7 % pts from the middle of last week --has led to the inversion of vol curves in a handful of major currencies (refer above chart). Coupled with palpable anxiety around the longevity of the unusually swift dollar downtrend, this vol structure is motivating considerations of short front vs. long back USD put calendar spreads as theta harvesting overlays on dollar shorts.

We are not convinced about the advisability of such structures however when realized vols are typically rising alongside a weakening dollar; the persistent forecasting error in recent weeks has been to underestimate the velocity of the dollar downtrend, and there is little evidence that consensus expectations have necessarily adjusted for these misses judging from the general surprise at yet another late-week drop in USDCNH.

The only currencies where one might consider sell/buy USD put calendars with some conviction are those where central banks have voiced concerns about FX strength and/or potentially defended a short-term floor (e.g. 1060 in USDKRW), but even there, powerful macro (trade-related appreciation pressures) and flow (equity inflows) forces could derail option constructs reliant on precise timing of spot moves. Courtesy: JPM