China’s Growth Faces Structural Challenges Amid Doubts Over Data

China’s Growth Faces Structural Challenges Amid Doubts Over Data  U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures

U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures  UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty

UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty  Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close

Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close  UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data

UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data  Nasdaq Proposes Fast-Track Rule to Accelerate Index Inclusion for Major New Listings

Nasdaq Proposes Fast-Track Rule to Accelerate Index Inclusion for Major New Listings  Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand

Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand  Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed

Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed  Stock Futures Dip as Investors Await Key Payrolls Data

Stock Futures Dip as Investors Await Key Payrolls Data  Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes

Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes  Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure

Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure  JPMorgan Lifts Gold Price Forecast to $6,300 by End-2026 on Strong Central Bank and Investor Demand

JPMorgan Lifts Gold Price Forecast to $6,300 by End-2026 on Strong Central Bank and Investor Demand  Geopolitical Shocks That Could Reshape Financial Markets in 2025

Geopolitical Shocks That Could Reshape Financial Markets in 2025  FxWirePro- Major Crypto levels and bias summary

FxWirePro- Major Crypto levels and bias summary

DXY tracking the U.S. unit against a basket of major currencies, fell 0.09 percent, with the euro also down 0.05 percent to $1.1862. FxWirePro’s currency strength index showing hourly USD performance is inching towards -117 levels (which is highly bearish), while hourly JPY spot index was at shy above 59 (bullish) while articulating (at 08:56 GMT).

Sterling was last trading at $1.3375, up 0.05 percent versus the greenback, while the Japanese yen strengthened 0.07 percent on the day.

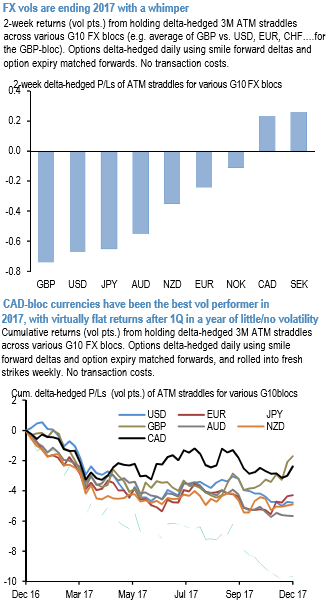

JPM’s USD index is a mere 0.1% stronger (though by way of a 1.3% range) despite substantial hurdles cleared in the US tax reform process, and a Fed rate hike.

The conviction of broad dollar forte through 1Q’2018 seems to be slightly pale as the greenback has failed to respond to the obvious rising probability of tax reform, disinflation uncertainty is weighing once more, and the Fed is not signaling acceleration in hikes for 2018 despite building in assumptions of fiscal stimulus. This implies any 1Q dollar strength might be much narrower and a greater likelihood that the range-bound and idiosyncratically driven conditions for the past month will spill over into 1Q18.

In this episode, we emphasize on predominant themes around which many 2018 outlook considerations engrossed:

1) Whether tax reform, the Fed, and/or repatriation could lift the dollar beyond intra-quarter bounces;

2) The comparative timing and feedthrough of policy normalization into FX; and

3) If markets were too sanguine on the US trade policy and EM backdrop.

Spot mean reversion: Before considering volatility surface parameters, the dynamics of the underlying FX rate come first. The DNT pay-off is fully path dependent, meaning that it does not depend on the FX level at the expiry but on its entire trajectory. The best possible path is obviously range-bound and mean reverting. To identify candidates, we rely on past spot dynamics and our FX forecasts.

While a range can break, a currency that is already range-bound is more likely to stay so compared to an already trending currency, which is less likely to suddenly consolidate. We are therefore interested in currencies displaying weak momentum. Technical analysis provides various momentum indicators that are useful when used dynamically. As we need an instantaneous picture of mean-reversion strength, we prefer to rely on econometrics and the more grounded stationarity concept, via an Augmented Dickey Fuller (ADF) test. Thus, we do not focus on currencies that are stationary, but the ADF statistic allows for quantifying the degree of strength by which a currency has recently mean reverted (refer above graph).

To this end, we compute ADF statistics for the past six months for daily FX rates data. The more the statistic is negative, the more the currency is mean reverting. Below -2.5, it is even stationary at a 10% threshold.

Volatility risk premium: To add DNTs, investors are keen on getting leverage in shorting volatility that the market is supposed to be overrating. ATM volatility (market volatility indicator) is considered in order to identify expensive implied volatilities in the same way as the options market, namely by comparing implied volatility to realized volatility.

While the above indicator provides a sophisticated comprehension of spot dynamics, the volatility risk premium compares the options market pricing to the spot dynamics. This indicator can be particularly useful for selecting rich expiries in the volatility term structure.

Selecting the same tenor for the implied and realized volatility is not the most efficient way to assess implied volatilities. Long-term realized volatilities are relatively insightful since the market tends to have a short-term memory, even for long tenors. Indeed, most of the volatility risk is integrated into the front end of the curve and is then more or less propagated towards the longer expires. In the same fashion, very-short-term volatilities are naturally unstable and are essentially useful for gamma trading. Empirically, we observe that the 3m realized volatility is the best sampling period for explaining implied volatilities all along the curve. Courtesy: SG

For more details on the FxWirePro’s currency strength index: please refer below weblink:

http://www.fxwirepro.com/currencyindex

FxWirePro launches Absolute Return Managed Program. For more details, visit: