Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure

Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure  SpaceX Earnings Preview: Bernstein Says 4 Key Factors Will Drive Long-Term Valuation

SpaceX Earnings Preview: Bernstein Says 4 Key Factors Will Drive Long-Term Valuation  Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand

Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand  European Stocks Rally on Chinese Growth and Mining Merger Speculation

European Stocks Rally on Chinese Growth and Mining Merger Speculation  S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays

S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays  Bank of America Posts Strong Q4 2024 Results, Shares Rise

Bank of America Posts Strong Q4 2024 Results, Shares Rise  US Gas Market Poised for Supercycle: Bernstein Analysts

US Gas Market Poised for Supercycle: Bernstein Analysts  China's Refining Industry Faces Major Shakeup Amid Challenges

China's Refining Industry Faces Major Shakeup Amid Challenges  ‘Vibe coding’ is fun and easy, but there’s a major catch

‘Vibe coding’ is fun and easy, but there’s a major catch  Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms

Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms  U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures

U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures  Moldova Criticizes Russia Amid Transdniestria Energy Crisis

Moldova Criticizes Russia Amid Transdniestria Energy Crisis  Same sparkle, different story: how lab-grown diamonds are transforming the market

Same sparkle, different story: how lab-grown diamonds are transforming the market

ECB extends asset purchases to end-2017: The monthly pace of purchases, however, will be reduced The ECB on 8 December announced that it would extend the end date of its asset purchase programme by nine months to the end of 2017, more than the six-month extension widely anticipated.

However, it also announced that from April it would reduce its monthly pace of purchases to €60bn from €80bn. The parameters of the programme will also change, enabling it to buy more short-dated securities, which helped to weaken the euro.

From January, the ECB will buy assets in the maturity range of 1-30yrs, compared with 2-30yrs previously, and also assets that yield below the deposit rate (-0.4%).

President Draghi sounded dovish and left open the possibility that asset purchases could be ramped up in the future if downside risks to economic growth materialise or underlying inflation fails to pick up. But if ‘core’ inflation does rise as projected, the ECB may start to wind down asset purchases from 2018.

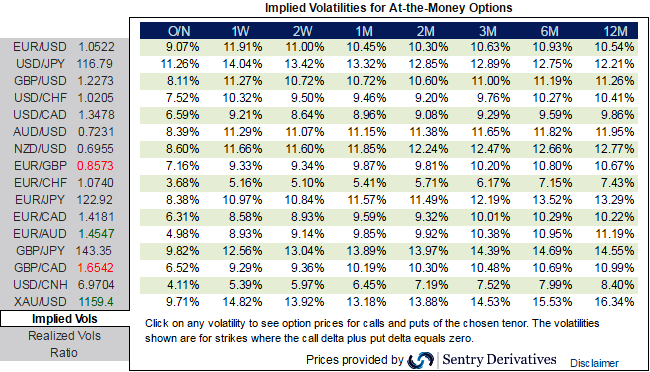

You see higher and steeper 6M-1Y EUR vols: you could make this out from the IV nutshell, rising hedging interests during this span.

Europe faced one constitutional referendum (Italy in December) and three to four national elections next year:

Netherlands in March, France in April/May, Germany by October and possibly Italy.

There are good reasons to think that eventual ballot box outcomes will buck the current populist trend and turn out Euro-benign.

Trump shock will now pull forward that time table, lift 6M-1Y expiry EUR vols that span European election dates, and bull-steepen the vol curve even if shorter- expiry implieds remain well-anchored by tight ranges on spot Euro.