China’s Growth Faces Structural Challenges Amid Doubts Over Data

China’s Growth Faces Structural Challenges Amid Doubts Over Data  Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close

Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close  BOJ Rate Hike Expectations Rise as Weak Yen and Strong U.S. Jobs Data Increase Pressure

BOJ Rate Hike Expectations Rise as Weak Yen and Strong U.S. Jobs Data Increase Pressure  Mexico's Undervalued Equity Market Offers Long-Term Investment Potential

Mexico's Undervalued Equity Market Offers Long-Term Investment Potential  Fed May Resume Rate Hikes: BofA Analysts Outline Key Scenarios

Fed May Resume Rate Hikes: BofA Analysts Outline Key Scenarios  BOJ Raises Interest Rates to 1% as Inflation Pressures Persist

BOJ Raises Interest Rates to 1% as Inflation Pressures Persist  Fed Chair Kevin Warsh Signals Policy Overhaul as Hawkish Rate Outlook Rattles Markets

Fed Chair Kevin Warsh Signals Policy Overhaul as Hawkish Rate Outlook Rattles Markets  Taiwan Central Bank Likely to Keep Interest Rates Unchanged Through 2027

Taiwan Central Bank Likely to Keep Interest Rates Unchanged Through 2027  Indonesia Plans Higher Asset Yields to Boost Rupiah and Restore Investor Confidence

Indonesia Plans Higher Asset Yields to Boost Rupiah and Restore Investor Confidence  Energy Sector Outlook 2025: AI's Role and Market Dynamics

Energy Sector Outlook 2025: AI's Role and Market Dynamics  ECB Set to Raise Interest Rates as Energy Shock Fuels Eurozone Inflation Concerns

ECB Set to Raise Interest Rates as Energy Shock Fuels Eurozone Inflation Concerns  S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays

S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays  Trump’s "Shock and Awe" Agenda: Executive Orders from Day One

Trump’s "Shock and Awe" Agenda: Executive Orders from Day One  New Zealand Unemployment and Inflation Debate Intensifies Ahead of 2026 Election

New Zealand Unemployment and Inflation Debate Intensifies Ahead of 2026 Election  RBA Minutes Signal Australia Central Bank Remains Ready to Raise Interest Rates if Inflation Persists

RBA Minutes Signal Australia Central Bank Remains Ready to Raise Interest Rates if Inflation Persists  China Sets 1.25% Overnight Reverse Repo Rate Below Market Expectations

China Sets 1.25% Overnight Reverse Repo Rate Below Market Expectations

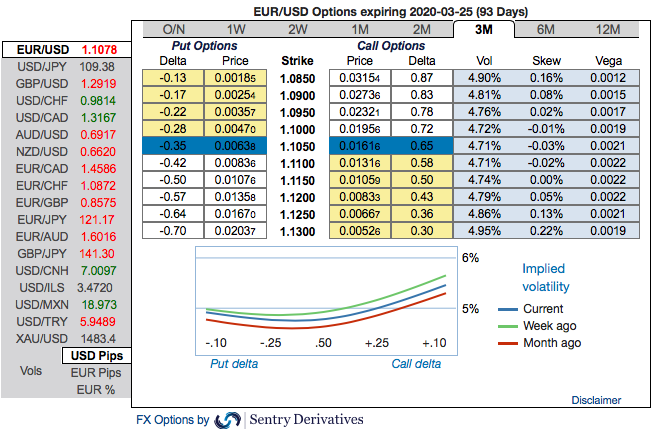

EURUSD (1Q’2020 1.12, 4Q’2020 1.14): The forecast envisages a belated lessening in cyclical headwinds that should enable a modest EUR recovery in line with the pull from cheap valuation and its record balance of payments support. Notably, EUR’s basic balance surplus has increased to 5.7% of GDP versus modest deficits in the US and Japan, helped by foreign inflows to Euro area equities in recent months. This underlying surplus should cushion the EUR against further cyclical disappointment and leverage it to genuine reflation.

FX Options Market Positioning:

The option market concurs with this asymmetry to judge from the positive EURUSD skew and so is the case with the risk reversal numbers. But skews are stretched towards both OTM puts and OTM calls. The EURUSD projection is rolled to 1.14 for end 2020, one cent upgrade to account for the lessening in cyclical tail risks and to reflect some hint of a US political risk premium in election year. But while EUR’s structural factors are compelling, they won’t fully compensate the currency should the economy continue to underwhelm. A meaningful EUR recovery requires economic reflation, evidence for which is so far inadequate to yet justify paying still hefty negative carry to own EUR outright.

EURUSD low IVs persisted despite the US Fed and ECB monetary policies in the recent past.

Anyone wanting to hedge against medium term exchange rate fluctuations will have to think twice whether writing options might not be the better strategy rather than buying options. Those who think so, the fear that the FX market will not develop the momentum ahead of Christmas to decide for one direction or the other.

Otherwise, 3M EURUSD IVs would hardly be stuck around the 4-5% mark and it has been prolonged. If one ignores GBP volatility though the FX market has returned to the vol lows seen last summer. The hopes are lingering that the vol levels seen at the time would be short-lived was correct in the sense that volatilities rose significantly in August.

However, there is no sustainable escape from the structural low volatility environment - that much has become clear. That is seemingly positive for all those for whom FX is an undesirable risk. IV factor is highly imperative in FX option dynamics because the option pricing significantly depends on future volatility, and it is quite impossible for any veteran to ascertain accurate future volatility.

Fiscal and Monetary Policy Impact:

Fiscal policy should turn supportive for EURUSD in 2020, not so much from a loosening in Euro area policy (this will add maybe 0.2- ppt to growth), but instead the end of Trump's Keynesian boom. While Monetary policy by contrast offers little respite from record-low vol in EURUSD but on balance should be supportive for spot. The Fed is tentatively on hold but biased to ease again whereas Lagarde’s ECB may be more cautious in expanding QE and exploring the ELB.

The overall risk bias is positive reflecting EUR’s strong structural fundamentals and US political risk

Hedging Strategies: Contemplating above factors, initiated long in 2 lots of EURUSD at the money -0.49 delta put options of 3M tenors, write an (1%) out of the money put option of 2w tenors, (spot reference: 1.1063 level). Short-legs go worthless as the underlying spot price hasn’t gone anywhere. Any slumps from here onwards are to be arrested by the 2 lots of ATM long-legs.

Those who are sceptic about mild rallies, 3m 1% in the money puts with attractive delta are advised on a hedging ground. Thereby, in the money put option with a very strong delta will move in tandem with the underlying.

Those who want to participate in the prevailing rallies in the short run, one can freshly initiate the strategy. The directional implementation of the same trading theme by further allow for a correlation-induced discount in the options trading also if you choose strikes appropriately. Courtesy: Sentrix & Saxobank