BOJ Hawk Signals Faster Interest Rate Hikes Amid Inflation Risks

BOJ Hawk Signals Faster Interest Rate Hikes Amid Inflation Risks  State of emergency in Crimea as Ukraine focuses pressure on ‘jewel in Putin’s crown’

State of emergency in Crimea as Ukraine focuses pressure on ‘jewel in Putin’s crown’  Japan Signals Surprise Yen Intervention Strategy as BOJ Hawkish Stance Puts FX Traders on Alert

Japan Signals Surprise Yen Intervention Strategy as BOJ Hawkish Stance Puts FX Traders on Alert  RBA Expected to Hold Interest Rates at 4.35% as Markets Watch AUD/USD and ASX 200

RBA Expected to Hold Interest Rates at 4.35% as Markets Watch AUD/USD and ASX 200  New Zealand Unemployment and Inflation Debate Intensifies Ahead of 2026 Election

New Zealand Unemployment and Inflation Debate Intensifies Ahead of 2026 Election  Taiwan Central Bank Likely to Keep Interest Rates Unchanged Through 2027

Taiwan Central Bank Likely to Keep Interest Rates Unchanged Through 2027  Gold Surges Past $4150 on Dovish Fed Signals and Weak Jobs Data; Bullish Outlook Prevails

Gold Surges Past $4150 on Dovish Fed Signals and Weak Jobs Data; Bullish Outlook Prevails  Buy the Dip: Gold Holds Strong at $3980, Targets $4150

Buy the Dip: Gold Holds Strong at $3980, Targets $4150  Elon Musk is remaking the world, like Henry Ford before him – but more dangerously

Elon Musk is remaking the world, like Henry Ford before him – but more dangerously  BOJ Raises Interest Rates to 1% as Inflation Pressures Persist

BOJ Raises Interest Rates to 1% as Inflation Pressures Persist

In BRICS FX bloc, ZAR weakness has probably run its course while the RUB benefited from the improving macro story in Russia and, more recently, from the firm recovery in oil prices with Brent bouncing above $55.

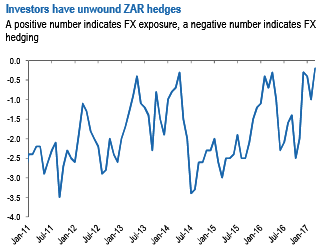

We expect USDZAR to settle around 13.5-14.00 in the days ahead as a base-case scenario. An overshoot is easily possible as investors have been increasing OWs and cutting FX hedges in recent weeks (refer above diagram).

We think a downgrade of local-currency ratings to junk is unlikely in the coming quarters. However, risks are that local-currency assets will not have much buffer against any policy deterioration going into 2018.

The HUF suffered the most in CEEMEA space, as the market discounted the sharply dovish stance of the MNB, which may use FX swap auctions to fine-tune liquidity and drive the currency lower.

In LatAm, the CLP strengthened the most, as other currencies remained pretty stable this week. The TWD and PHP took the lead in East Asia, benefiting from better US/China relations, Trump being vocal about the dollar being excessively strong, and boosted by a World Bank report raising the local forecast growth profile.

In Mexico, we still favor calendar skews and hold to our short-term view that more attractive carry-to-volatility ratios could drive speculative positioning to further correct, with USDMXN likely converging to the 18.2-18.6 range, all else equal.

We remain wary of both NAFTA negotiations and domestic political risk in H2’17, so we recommend positioning for near-term performance in MXN followed by a weaker H2 via 1m vanilla options. Next week, the Trump-Xi meeting could cast light of US trade strategy going forward, and could reverberate on USDMXN.